Barclays Bank PLC - iPath® Series B S&P 500® VIX Short-Term FuturesTM ETN

VXX

34.70

-0.03

(-0.09%)

7:59:56 PM EDT: $34.92 +0.22 (+0.63%)

The Incredible Option Trade in VXX That Keeps Winning

Preface

The iPath S&P 500 VIX Short Term Futures TM ETN (NYSEARCA:VXX) is casually referred to as "the VXX.". That likely means nothing to you. In English, the obligation of the VXX is to match the performance of the S&P 500 VIX Short-Term Futures Index Total Return and that is a strategy index which maintains positions in the front two-month CBOE Volatility Index (VIX) futures contracts.

WHAT?

A quick step back before we thrust forward. The VIX that we see on CNBC or various websites is actually called the 'Spot VIX' and it is not a tradeable asset -- which is to say, you cannot buy or sell the VIX spot.

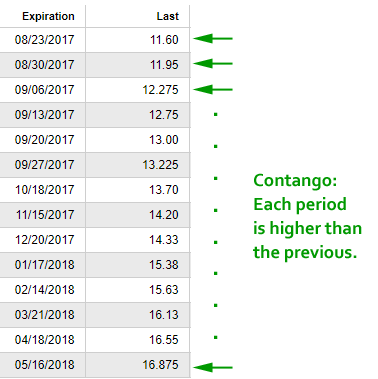

The VIX spot is derived from the implied volatility of SPX options. But the tradeable VIX is actually in the futures market. Here is how VIX futures look as of 8-22-2017, pay special attention to the price for each expiry, and how it rises with each successive date.

We can see a futures expiration every week through 9-27-2017, and then it goes monthly. But that's not the key, here.

Notice that for every time period further out in the future, the price of the VIX future is higher than the last. This pattern, when the future price is higher than the price behind it, is called "contango." The opposite, for those curious, is called "backwardation."

BACK TO THE VXX

Jill Malandrino, formerly of TheStreet.com writes it beautifully when she notes:

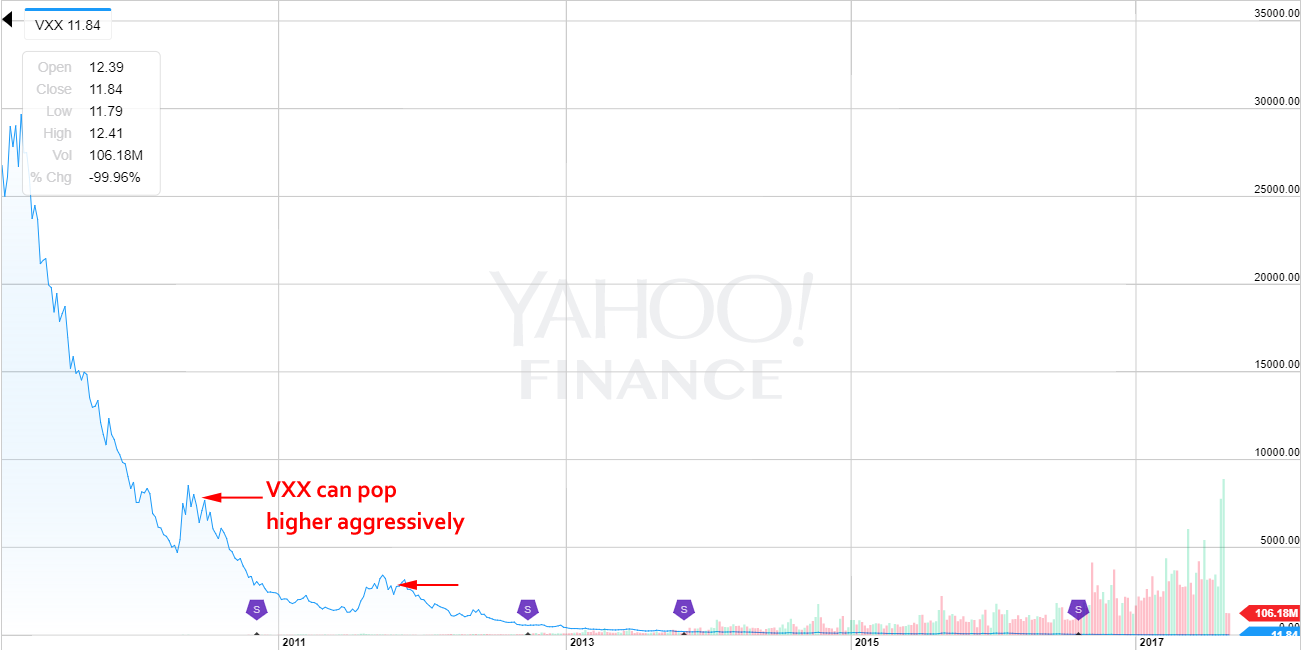

To see how often VIX futures are in contango, or more precisely, how often VXX falls, here is an all-time price chart for VXX:

Yep, the VXX is down 99.96% since inception. The reason is simply that VIX is almost always in contango. For the times that VIX falls out of contango, we can see abrupt pops in the VXX which we have highlighted in the image above.

Note that the VXX does a reverse split quite often and that's why it isn't trading at $0.01. It splits into fewer shares which raises the stock price -- obviously having no affect on the actual option trade. The most recent split is 8-23-2017.

OK - TALK TO ME ABOUT THE TRADE

For those that want more information on the VXX and VIX futures the CBOE is a treasure trove of information as is Jill's article 5 Misperceptions About VXX.

With the price of VXX trending down most of the time, except for rare instances where there are large price spikes, a simple option strategy should work.

TRADING VXX

We tested buying an a put spread in the VXX using the 90 day options over the last five-years. Here are those results:

Tap Here to See the back-test

We see a 615% return, testing this over the last 5-years. Since we tested the 90 day options, that was 21 trades, in which 17 were winners and 4 were losers.

We can see that this strategy hasn't been a winner all the time, but it has won a lot.

Setting Expectations

While this strategy has an overall return of 615%, the trade details keep us in bounds with expectations:

➡ The average percent return per trade was 28.9% (in 90 days).

➡ The average percent return per winning trade was 52.7% (in 90 days).

➡ The average percent return per losing trade was -72.4% (in 90 days).

We note that when the VIX goes into backwardation, the VXX does pop aggressively higher and we see that in the average loss, which is actually larger than the average win.

Option Trading in the Last Year

We can also look at the last year of trading in the VXX

Tap Here to See the back-test

The results are staggeringly similar to the five-year results with a 80% win-rate versus the 81% win-rate over 5-years.

➡ Over just the last year, the average percent return per trade was 50.3% (in 90 days).

➡ The average percent return per winning trade was 63.4% (in 90 days).

➡ The percent return for the one losing trade was -1.9% (in 90 days).

The key to this trade has been risk control so the losses aren't harmful and didn't discourage trading the next cycle.

If you like what you're reading, learn more about scientific option trading in a free webinar we are holding:

Discover the power of applying science to your options trading in a free webinar:

Discover Scientific Options Trading

WHAT HAPPENED

Successful option trading is about preparation -- it's methodical -- it's scientific. This is it -- this is how people profit from the option market, and this can be done with any stock, ETF, ETN or index.

To see how to become a scientific option trader and take the guess work out, we welcome you to watch this quick demonstration video:

Tap Here to See the Tools at Work

Thanks for reading.

Risk Disclosure

You should read the Characteristics and Risks of Standardized Options.

Past performance is not an indication of future results.

Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.

{kind=link}

The Incredible Option Trade in VXX That Keeps Winning

VXX

Date Published: 2017-08-22Author: Ophir Gottlieb

Preface

The iPath S&P 500 VIX Short Term Futures TM ETN (NYSEARCA:VXX) is casually referred to as "the VXX.". That likely means nothing to you. In English, the obligation of the VXX is to match the performance of the S&P 500 VIX Short-Term Futures Index Total Return and that is a strategy index which maintains positions in the front two-month CBOE Volatility Index (VIX) futures contracts.

WHAT?

A quick step back before we thrust forward. The VIX that we see on CNBC or various websites is actually called the 'Spot VIX' and it is not a tradeable asset -- which is to say, you cannot buy or sell the VIX spot.

The VIX spot is derived from the implied volatility of SPX options. But the tradeable VIX is actually in the futures market. Here is how VIX futures look as of 8-22-2017, pay special attention to the price for each expiry, and how it rises with each successive date.

We can see a futures expiration every week through 9-27-2017, and then it goes monthly. But that's not the key, here.

Notice that for every time period further out in the future, the price of the VIX future is higher than the last. This pattern, when the future price is higher than the price behind it, is called "contango." The opposite, for those curious, is called "backwardation."

BACK TO THE VXX

Jill Malandrino, formerly of TheStreet.com writes it beautifully when she notes:

This has a negative impact on VXX as the strategy VXX was created to follow will consistently sell front-month futures and buy second-month futures.

This buying and selling of futures contracts is done to maintain a 30-day weighting between the two. Often this means that cheaper futures are being sold and more expensive futures being purchased. Eventually the second month future becomes the front month and the strategy will sell those contracts and begin purchasing the farther month.

Often when selling commences the price of the future is lower than when it was purchased and the vast majority of the time the front month is being sold for less premium than is being paid for second month.

This buying and selling of futures contracts is done to maintain a 30-day weighting between the two. Often this means that cheaper futures are being sold and more expensive futures being purchased. Eventually the second month future becomes the front month and the strategy will sell those contracts and begin purchasing the farther month.

Often when selling commences the price of the future is lower than when it was purchased and the vast majority of the time the front month is being sold for less premium than is being paid for second month.

To see how often VIX futures are in contango, or more precisely, how often VXX falls, here is an all-time price chart for VXX:

Yep, the VXX is down 99.96% since inception. The reason is simply that VIX is almost always in contango. For the times that VIX falls out of contango, we can see abrupt pops in the VXX which we have highlighted in the image above.

Note that the VXX does a reverse split quite often and that's why it isn't trading at $0.01. It splits into fewer shares which raises the stock price -- obviously having no affect on the actual option trade. The most recent split is 8-23-2017.

OK - TALK TO ME ABOUT THE TRADE

For those that want more information on the VXX and VIX futures the CBOE is a treasure trove of information as is Jill's article 5 Misperceptions About VXX.

With the price of VXX trending down most of the time, except for rare instances where there are large price spikes, a simple option strategy should work.

TRADING VXX

We tested buying an a put spread in the VXX using the 90 day options over the last five-years. Here are those results:

| VXX Long 50/30 Delta Put Spread |

|||

| % Wins: | 81% | ||

| Wins: 17 | Losses: 4 | ||

| % Return: | 615% | ||

Tap Here to See the back-test

We see a 615% return, testing this over the last 5-years. Since we tested the 90 day options, that was 21 trades, in which 17 were winners and 4 were losers.

We can see that this strategy hasn't been a winner all the time, but it has won a lot.

Setting Expectations

While this strategy has an overall return of 615%, the trade details keep us in bounds with expectations:

➡ The average percent return per trade was 28.9% (in 90 days).

➡ The average percent return per winning trade was 52.7% (in 90 days).

➡ The average percent return per losing trade was -72.4% (in 90 days).

We note that when the VIX goes into backwardation, the VXX does pop aggressively higher and we see that in the average loss, which is actually larger than the average win.

Option Trading in the Last Year

We can also look at the last year of trading in the VXX

| VXX Long 50/30 Delta Put Spread |

|||

| % Wins: | 80% | ||

| Wins: 4 | Losses: 1 | ||

| % Return: | 138% | ||

Tap Here to See the back-test

The results are staggeringly similar to the five-year results with a 80% win-rate versus the 81% win-rate over 5-years.

➡ Over just the last year, the average percent return per trade was 50.3% (in 90 days).

➡ The average percent return per winning trade was 63.4% (in 90 days).

➡ The percent return for the one losing trade was -1.9% (in 90 days).

The key to this trade has been risk control so the losses aren't harmful and didn't discourage trading the next cycle.

If you like what you're reading, learn more about scientific option trading in a free webinar we are holding:

Discover the power of applying science to your options trading in a free webinar:

Discover Scientific Options Trading

WHAT HAPPENED

Successful option trading is about preparation -- it's methodical -- it's scientific. This is it -- this is how people profit from the option market, and this can be done with any stock, ETF, ETN or index.

To see how to become a scientific option trader and take the guess work out, we welcome you to watch this quick demonstration video:

Tap Here to See the Tools at Work

Thanks for reading.

Risk Disclosure

You should read the Characteristics and Risks of Standardized Options.

Past performance is not an indication of future results.

Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.