Oracle Corp.

XNYS:ORCL 4:00:00 PM EDT

155.97

+0.86

(+0.55%)

7:59:38 PM EDT: $155.65 -0.32 (-0.21%)

Oracle Corporation, ORCL, earnings, option, swing, short-term

Preface

Just as earnings season comes to an end, the next one is just around the corner. We turn to a tech giant that has shown the pattern of bullish momentum in days leading up to earnings.

This is a short-term swing trade, it won't be a winner forever, and it can be easily derailed by a couple of down days in the market irrespective of Oracle Corporation news, but for now it has shown a repeating success that has not only returned 355% annualized returns, but has also shown a win-rate of 83% in the last three-years and 87.5% in the last two-years.

DISCOVERY

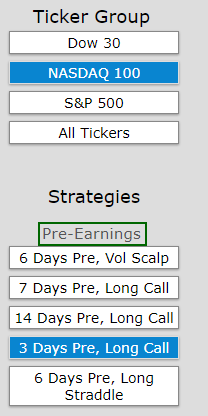

I discovered this scan from the CML Trade Machine Pro scanner, looking for momentum trades in the NASDAQ 100 that had earnings due soon.

Here's what I found:

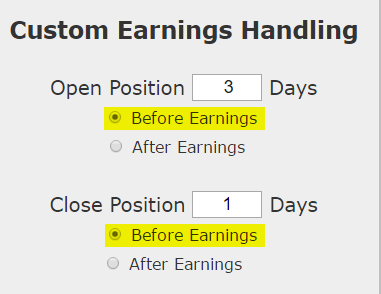

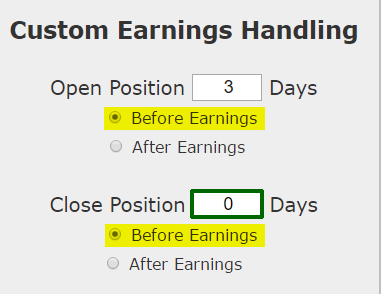

Then I went to the back-test and changed the timing from this:

To this:

Notice the subtle difference -- since Oracle historically reports earnings after the close, we could push the trade one further day and close on earnings day, but right before the close, so no actual earnings risk is being taken. Also, given Oracle's recent efforts to move more aggressively into the cloud, perhaps this pre-earnings optimism is warranted.

It's a good reminder that it is in the intersection of computing power / machine learning and human experience where some of the best analysis comes from.

IDEA

The idea is quite simple -- trying to take advantage of a pattern in short-term bullishness just before earnings, and then getting out of the way so no actual earnings risk is taken. Now we can see it in Oracle Corporation.

The Short-term Option Swing Trade Ahead of Earnings in Oracle Corporation

We will examine the outcome of going long a weekly call option in Oracle Corporation just three calendar days before earnings and selling the call on the day of the actual news but before the earnings report.

This is construct of the trade, noting that the short-term trade closes before earnings and therefore does not take a position on the earnings result.

We note that the earnings date estimate for Oracle is 9-14-2017, but this date is not confirmed, yet. So this requires a check back in a few days to get a solid date.

Often times we look at option set-ups that are longer-term, and take no directional bet -- this is not one of those times. This is a no holds barred short-term bullish swing trade with options and that's it. It's a bullish bet, so must be conscious of the delta risk.

RISK MANAGEMENT

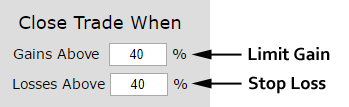

We can add another layer of risk management to the back-test by instituting and 40% stop loss and a 40% limit gain. Here is that setting:

In English, at the close of each trading day we check to see if the long option is either up or down 40% relative to the open price. If it was, the trade was closed.

RESULTS

Below we present the back-test stats over the last three-years in Oracle Corporation:

Tap Here to See the Back-test

We see a 355% return, testing this over the last 12 earnings dates in Oracle Corporation. That's a total of just 36 days (3-day holding period for each earnings date, over 12 earnings dates). That's the power of following the short-term pattern of bullishness ahead earnings -- and not taking on the actual risk from the earnings outcome.

The trade will lose sometimes, and since it is such a short-term position, it can lose from news that moves the whole market that has nothing to do with Oracle Corporation, but over the recent history, this bullish option trade has won ahead of earnings.

Setting Expectations

While this strategy has an overall return of 355%, the trade details keep us in bounds with expectations:

➡ The average percent return per trade was 34.7% over just three-days.

➡ The average percent return per winning trade was 46%.

➡ The average percent return per losing trade was -21.6%.

Looking at More Recent History

We did a multi-year back-test above, now we can look at just the last year:

We're now looking at 105% returns, on 3 winning trades and 1 losing trades.

➡ The average percent return over the last year per trade was 26.8% over just three-days.

➡ The average percent return per winning trade was 36.5%.

➡ The average percent return for the one losing trade was -2%.

WHAT HAPPENED

Bull markets tend to create optimism, whether it's deserved or not. This has been a tradable phenomenon in Oracle Corporation. To see how to test this for any stock we welcome you to watch this quick demonstration video:

Tap Here to See the Tools at Work

Risk Disclosure

You should read the Characteristics and Risks of Standardized Options.

Past performance is not an indication of future results.

Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.

{kind=link}

Swing Trading Earnings Bullish Momentum With Options in Oracle Corporation

Oracle Corporation (NYSE:ORCL) : Swing Trading Earnings Bullish Momentum With Options

Date Published: 2017-09-3Author: Ophir Gottlieb

Preface

Just as earnings season comes to an end, the next one is just around the corner. We turn to a tech giant that has shown the pattern of bullish momentum in days leading up to earnings.

This is a short-term swing trade, it won't be a winner forever, and it can be easily derailed by a couple of down days in the market irrespective of Oracle Corporation news, but for now it has shown a repeating success that has not only returned 355% annualized returns, but has also shown a win-rate of 83% in the last three-years and 87.5% in the last two-years.

DISCOVERY

I discovered this scan from the CML Trade Machine Pro scanner, looking for momentum trades in the NASDAQ 100 that had earnings due soon.

Here's what I found:

Then I went to the back-test and changed the timing from this:

To this:

Notice the subtle difference -- since Oracle historically reports earnings after the close, we could push the trade one further day and close on earnings day, but right before the close, so no actual earnings risk is being taken. Also, given Oracle's recent efforts to move more aggressively into the cloud, perhaps this pre-earnings optimism is warranted.

It's a good reminder that it is in the intersection of computing power / machine learning and human experience where some of the best analysis comes from.

IDEA

The idea is quite simple -- trying to take advantage of a pattern in short-term bullishness just before earnings, and then getting out of the way so no actual earnings risk is taken. Now we can see it in Oracle Corporation.

The Short-term Option Swing Trade Ahead of Earnings in Oracle Corporation

We will examine the outcome of going long a weekly call option in Oracle Corporation just three calendar days before earnings and selling the call on the day of the actual news but before the earnings report.

This is construct of the trade, noting that the short-term trade closes before earnings and therefore does not take a position on the earnings result.

We note that the earnings date estimate for Oracle is 9-14-2017, but this date is not confirmed, yet. So this requires a check back in a few days to get a solid date.

Often times we look at option set-ups that are longer-term, and take no directional bet -- this is not one of those times. This is a no holds barred short-term bullish swing trade with options and that's it. It's a bullish bet, so must be conscious of the delta risk.

RISK MANAGEMENT

We can add another layer of risk management to the back-test by instituting and 40% stop loss and a 40% limit gain. Here is that setting:

In English, at the close of each trading day we check to see if the long option is either up or down 40% relative to the open price. If it was, the trade was closed.

RESULTS

Below we present the back-test stats over the last three-years in Oracle Corporation:

| ORCL: Long 40 Delta Call | |||

| % Wins: | 83.3% | ||

| Wins: 10 | Losses: 2 | ||

| % Return: | 355% | ||

Tap Here to See the Back-test

We see a 355% return, testing this over the last 12 earnings dates in Oracle Corporation. That's a total of just 36 days (3-day holding period for each earnings date, over 12 earnings dates). That's the power of following the short-term pattern of bullishness ahead earnings -- and not taking on the actual risk from the earnings outcome.

The trade will lose sometimes, and since it is such a short-term position, it can lose from news that moves the whole market that has nothing to do with Oracle Corporation, but over the recent history, this bullish option trade has won ahead of earnings.

Setting Expectations

While this strategy has an overall return of 355%, the trade details keep us in bounds with expectations:

➡ The average percent return per trade was 34.7% over just three-days.

➡ The average percent return per winning trade was 46%.

➡ The average percent return per losing trade was -21.6%.

Looking at More Recent History

We did a multi-year back-test above, now we can look at just the last year:

We're now looking at 105% returns, on 3 winning trades and 1 losing trades.

➡ The average percent return over the last year per trade was 26.8% over just three-days.

➡ The average percent return per winning trade was 36.5%.

➡ The average percent return for the one losing trade was -2%.

WHAT HAPPENED

Bull markets tend to create optimism, whether it's deserved or not. This has been a tradable phenomenon in Oracle Corporation. To see how to test this for any stock we welcome you to watch this quick demonstration video:

Tap Here to See the Tools at Work

Risk Disclosure

You should read the Characteristics and Risks of Standardized Options.

Past performance is not an indication of future results.

Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.