SSgA Active Trust - Financial Select Sector SPDR

XLF

53.19

+0.57

(+1.08%)

4:59:06 PM EDT: $53.20 +0.01 (+0.02%)

XLF, Financial, Rotation, call

Disclaimer

The results here are provided for general informational purposes, as a convenience to the readers. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation.

Preface

A rotation has begun from technology into financials -- that's what the headlines would have us believe. But the truth is, rotation or not, a simple option strategy has returned nearly 1,600% over the last five-years in the Financial Select Sector SPDR Fund (NYSEARCA:XLF) with a 75% win rate. It's this back-test we will discuss today.

IDEA

The idea is a bit more involved than a straight down the middle bullish back-test -- it is a rolling call calendar spread.

The Weekly Call Calendar in Financial Select Sector SPDR Fund (NYSEARCA:XLF)

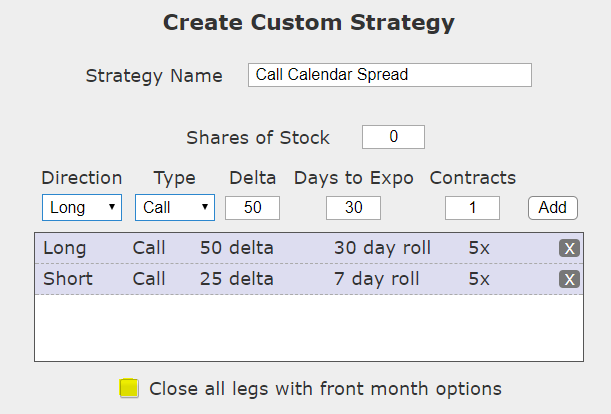

We will examine the outcome of going long a monthly at-the-money call option (also called '50-delta call option') and selling an out-of-the-money call option (25 delta) every week. Here is how to create this strategy in Trade Machine Pro using the custom strategy button:

Explicitly, this back-test measures the results of going long a monthly option and selling a weekly option against it. The "close all legs with front month options" check box is unchecked, that is, we let the weekly options expire and leave the monthly options alone.

RESULTS

Below we present the back-test results over the last five-years in XLF. During this time period the ETF was up 134.3%.

Tap Here to See the Back-test

The mechanics of the TradeMachine™ are that it uses end of day prices for every back-test entry and exit (every trigger).

We see a 1595% return, testing this over the last five-years, and it is a fairly active trade that rolls every week with one of the legs.

Setting Expectations

While this strategy has an overall return of 1595%, the trade details keep us in bounds with expectations:

➡ The average percent return per winning trade was 72.6%.

➡ The average percent return per losing trade was -77.3%.

The trade simply won 3 times every 4 weeks.

Looking at More Recent History

We did a multi-year back-test above, now we can look at just the last year:

Tap Here to See the Back-test

We note that over the last year we see a win rate that is a little bit higher than the total five-year test, so yes, the 'rotation' story is taking hold, but this back-test has consistent results over the last 5-years as well, so if the rotation story fades, it does not necessarily imply a large impact on the back-test.

WHAT HAPPENED

Option trading isn't about luck, it's about empirical and explicit testing. To see how to test this for any stock and any strategy, we welcome you to watch this quick demonstration video:

Tap Here to See the Tools at Work

Risk Disclosure

You should read the Characteristics and Risks of Standardized Options.

Past performance is not an indication of future results.

Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.

Please note that the executions and other statistics in this article are hypothetical, and do not reflect the impact, if any, of certain market factors such as liquidity and slippage.

{kind=link}

{kind=link}

XLF: How to Trade the Great Financial Rotation With Options

XLF: How to Trade the Great Financial Rotation With Options

Date Published: 2017-12-12Author: Ophir Gottlieb

Disclaimer

The results here are provided for general informational purposes, as a convenience to the readers. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation.

Preface

A rotation has begun from technology into financials -- that's what the headlines would have us believe. But the truth is, rotation or not, a simple option strategy has returned nearly 1,600% over the last five-years in the Financial Select Sector SPDR Fund (NYSEARCA:XLF) with a 75% win rate. It's this back-test we will discuss today.

IDEA

The idea is a bit more involved than a straight down the middle bullish back-test -- it is a rolling call calendar spread.

The Weekly Call Calendar in Financial Select Sector SPDR Fund (NYSEARCA:XLF)

We will examine the outcome of going long a monthly at-the-money call option (also called '50-delta call option') and selling an out-of-the-money call option (25 delta) every week. Here is how to create this strategy in Trade Machine Pro using the custom strategy button:

Explicitly, this back-test measures the results of going long a monthly option and selling a weekly option against it. The "close all legs with front month options" check box is unchecked, that is, we let the weekly options expire and leave the monthly options alone.

RESULTS

Below we present the back-test results over the last five-years in XLF. During this time period the ETF was up 134.3%.

| XLF: Call Calendar Spread |

|||

| % Wins: | 75.1% | ||

| Wins: 190 | Losses: 63 | ||

| % Return: | 1595% | ||

Tap Here to See the Back-test

The mechanics of the TradeMachine™ are that it uses end of day prices for every back-test entry and exit (every trigger).

We see a 1595% return, testing this over the last five-years, and it is a fairly active trade that rolls every week with one of the legs.

Setting Expectations

While this strategy has an overall return of 1595%, the trade details keep us in bounds with expectations:

➡ The average percent return per winning trade was 72.6%.

➡ The average percent return per losing trade was -77.3%.

The trade simply won 3 times every 4 weeks.

Looking at More Recent History

We did a multi-year back-test above, now we can look at just the last year:

| XLF: Call Calendar Spread |

|||

| % Wins: | 77.4% | ||

| Wins: 41 | Losses: 12 | ||

| % Return: | 809% | ||

Tap Here to See the Back-test

We note that over the last year we see a win rate that is a little bit higher than the total five-year test, so yes, the 'rotation' story is taking hold, but this back-test has consistent results over the last 5-years as well, so if the rotation story fades, it does not necessarily imply a large impact on the back-test.

WHAT HAPPENED

Option trading isn't about luck, it's about empirical and explicit testing. To see how to test this for any stock and any strategy, we welcome you to watch this quick demonstration video:

Tap Here to See the Tools at Work

Risk Disclosure

You should read the Characteristics and Risks of Standardized Options.

Past performance is not an indication of future results.

Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.

Please note that the executions and other statistics in this article are hypothetical, and do not reflect the impact, if any, of certain market factors such as liquidity and slippage.