Roku Inc - Ordinary Shares - Class A

NASDAQ:ROKU 12:23:51 AM EDT

58.05

-0.89

(-1.51%)

roku, year, million, company, streaming, revenue, platform, video

Written by Ophir Gottlieb

This is a snippet from a CML Pro dossier published on 2-22-2018.

LEDE

ROKU released earnings after the close of the market on 2-21-2018, and while the market has pushed the stock down, the results, in our option, were breathtakingly good.

Our thesis for the company can be reviewed in the Top Pick dossier: The Tech Gem Looking to Dominate Streaming Video.

STORY

ROKU is building a business based on users and if we measured them as a cable provider, as of right now, they would be the third largest cable provider in the country behind just Comcast and AT&T -- that's how many people and how much content they serve, already.

Further, the number of accounts for ROKU rose 44% while Comcast and AT&T are essentially flat. All of this is driven by the large secular shift by consumers to streaming video and away from linear TV.

Check out this video consumption pattern forecast:

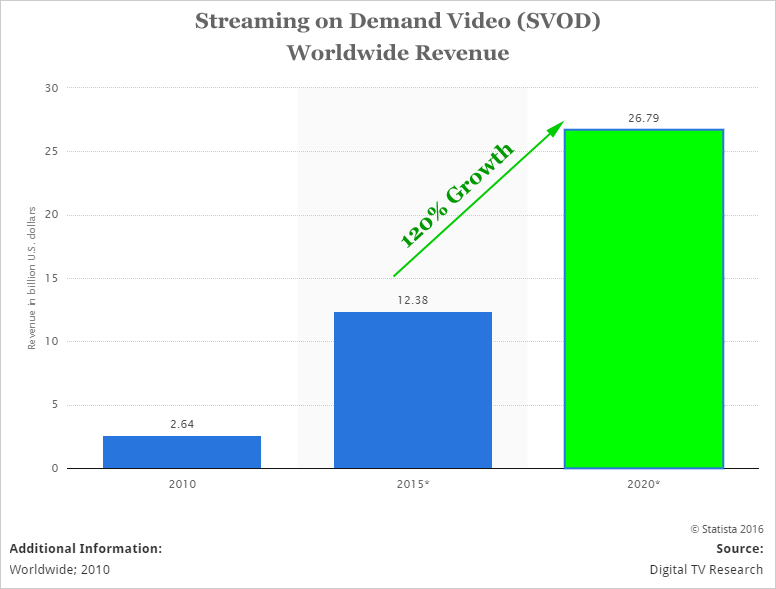

And then straight to SVOD revenue forecasts.

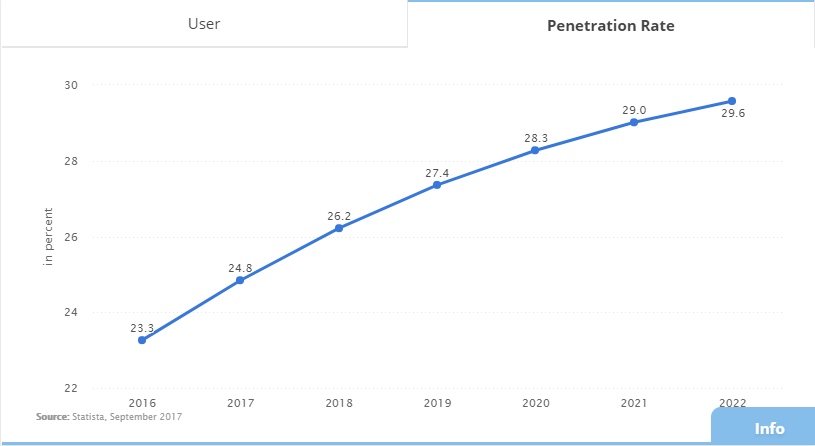

The penetration rate of streaming video is growing in the United States, but is still below 25%:

The various SVOD content providers are in a war - to buy content, to buy users, to keep users, to differentiate. Netflix, Amazon Prime Video and Hulu are at war with each other, as they are with other over the top (OTT) video services like those coming from Apple, Google (YouTube), Disney, and many others.

That battle doesn't interest us - what we are after is the operating system, the guts, that will house all of it. And this is where Roku exists. Each of these over the top (OTT) content providers are available with Roku hardware or software.

The idea behind the business is to grow scale -- to grow active accounts, and to become the operating system of streaming TV. Yes, their goal, their future, is to be what Microsoft was to PCs and what Apple is to smartphones -- the platform, the operating system, for the booming industry that is Streaming Video on Demand (SVOD).

Or, as the CEO said in the earnings call:

And the company has done so in spades. Not only did ROKU reported a stunning 44% growth in account accounts in Q4, but also an average revenue per user (ARPU) growth of 48%. These are gigantic numbers.

The CEO said, on the earnings call (our emphasis added):

While the company's hardware revenue was down, and that has Wall Street spooked, that was very much on purpose. As the CEO said out loud on CNBC, the company lowered prices on its players to increase volume. It's still a gross margin positive business, but hardware is simply one conduit to more users.

Executives cut the price for one of Roku's top-end models to $100 from $130, for example, and released a budget $30 version called the Roku Express. Again, this was done on purpose. Hardware is a customer-acquisition strategy, not a profit center in and of itself.

Even further, the company noted that for the first time, platform revenue will make up the majority of the company's overall revenue throughout 2018. In fact, platform gross profit grew 120% year-over-year to $63.7 million and represented 87% of total gross profit in Q4, up from 65% last year.

The company gets new users by selling players, licensing players and licensing the operating system. As for other financial metrics, the company's guidance, at its mid-point, is a gross profit rise of fully 56% year-over-year.

Roku's license sources delivered more than half of the company's new user growth in the fourth quarter.

ROKU has access to treasure trove of data and as a distributor of content and an advertiser, data is a key part of that business in the modern world. While ad revenue and content redistribution revenue are the focus, the data behind it is extremely powerful and is a moat that a linear TV cable provider simply does not have.

Think about this, and this is straight from the CEO: "Every ad on ROKU is a one-on-one ad targeted to that specific customer." Now, compare that to cable TV. It's almost an unfair advantage that streaming has over linear television, but there it is.

And the results: advertising remains the largest component of platform revenue, accounting for 75% of that segment, versus 66% in the previous quarter. As for scale, try this on for size:

U.S advertisers spend $70 billion a year on TV, according to ROKU CEO Anthony Wood.

Or how about this: four-years ago ROKU had 0% of the market, and as of last year 1 out of every 5 televisions used the ROKU operating system for streaming. This is much more of a software company than a hardware company, irrespective of where revenue sits today.

Now, let's turn to the earnings results and the earnings call:

EARNINGS

* Revenue: $188.3 million from $147.3 million in the year-ago period, beating analysts' average expectations of $182.5 million.

* EPS: $0.06 profit versus analyst expectations of a -$0.10 per share loss million from $147.3 million in the year-ago period, beating analysts' average expectations of $182.5 million.

* Guidance: Full year revenue of $660 million to $690 million versus estimates of $661.5 million.

Full year losses of $40 million to $55 million versus analyst expectations of $35.9 million.

EARNINGS CALL

Here are the highlights we focused on:

* The shift to streaming is creating huge opportunities for Roku.

* Active accounts grew 44% for the year.

* ARPU increased 48% year-over-year to $13.78 on a trailing 12-month basis with more than two-thirds of ARPU coming from advertising.

* The largest driver of ARPU growth is video advertising.

* We are also seeing very rapid growth from our audience development ads which are endemic display ads.

* Our Roku TV program had exceptional performance, one in five smart TV sold in the U.S in 2017 were Roku TV.

* Our investment and being the leading TV OS is paying off.

* We're increasingly tapping into the $70 billion [] U.S advertisers spend on TV as the TV ad ecosystem moves to streaming.

* More than half of the Ad Age's top 200 advertise on the Roku platform.

* Q4 gross profit increased 64% year-over-year to $73.5 million.

* Platform gross profit grew 120% year-over-year to $63.7 million and represented 87% of total gross profit in Q4, up from 65% last year.

CONCLUSION

We loved the quarter ROKU had, see quite clearly that its actual hardware, which still turns a profit, is not the focus other than as a conduit to get its operating system out there and its account numbers up.

Combine that hardware effort with licensing, and ROKU's growth is something to behold in a cable industry that is flat, at best, and shrinking at worst. Yes, ROKU saw 44% account growth as the cable providers are seeing cord cutting hurt their business.

Advertising is a fantastic business -- just ask Google (the largest advertising platform in the world and the second largest company in the world by market cap) and Facebook (the second largest ad platform in the world and the sixth largest company by market cap in the world).

SEEING THE FUTURE

It's understanding technology that gets us an edge on finding the gems like ROKU that can turn into the 'next Apple,' or 'next Microsft,' where we must get ahead of the curve. This is what CML Pro does.

We are Capital Market Laboratories. Our research sits next to Goldman Sachs, JP Morgan, Barclays, Morgan Stanley and every other multi billion dollar institution as a member of the famed Thomson Reuters First Call. But while those people pay upwards of $2,000 a month on their live terminals, we are the anti-institution and are breaking the information asymmetry.

The precious few thematic top picks for 2018, research dossiers, and alerts are available for a limited time at a 80% discount for $29/mo. Join Us: Discover the undiscovered companies that will power technology's future.

As always, control risk, size appropriately and use your own judgement, aside from anyone else's subjective views, including my own.

Thanks for reading, friends.

The author has no position in ROKU but may initiate one within 72-hours.

Legal

The information contained on this site is provided for general informational purposes, as a convenience to the readers. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation. Consult the appropriate professional advisor for more complete and current information. Capital Market Laboratories ("The Company") does not engage in rendering any legal or professional services by placing these general informational materials on this website.

The Company specifically disclaims any liability, whether based in contract, tort, strict liability or otherwise, for any direct, indirect, incidental, consequential, or special damages arising out of or in any way connected with access to or use of the site, even if we have been advised of the possibility of such damages, including liability in connection with mistakes or omissions in, or delays in transmission of, information to or from the user, interruptions in telecommunications connections to the site or viruses.

The Company make no representations or warranties about the accuracy or completeness of the information contained on this website. Any links provided to other server sites are offered as a matter of convenience and in no way are meant to imply that The Company endorses, sponsors, promotes or is affiliated with the owners of or participants in those sites, or endorse any information contained on those sites, unless expressly stated.

{kind=link}

ROKU's Bullish Thesis is Getting Yet Stronger

ROKU's Bullish Thesis is Getting Yet Stronger

Date Published: 2018-02-26Author: Ophir Gottlieb

Written by Ophir Gottlieb

This is a snippet from a CML Pro dossier published on 2-22-2018.

LEDE

ROKU released earnings after the close of the market on 2-21-2018, and while the market has pushed the stock down, the results, in our option, were breathtakingly good.

Our thesis for the company can be reviewed in the Top Pick dossier: The Tech Gem Looking to Dominate Streaming Video.

STORY

ROKU is building a business based on users and if we measured them as a cable provider, as of right now, they would be the third largest cable provider in the country behind just Comcast and AT&T -- that's how many people and how much content they serve, already.

Further, the number of accounts for ROKU rose 44% while Comcast and AT&T are essentially flat. All of this is driven by the large secular shift by consumers to streaming video and away from linear TV.

Check out this video consumption pattern forecast:

And then straight to SVOD revenue forecasts.

The penetration rate of streaming video is growing in the United States, but is still below 25%:

The various SVOD content providers are in a war - to buy content, to buy users, to keep users, to differentiate. Netflix, Amazon Prime Video and Hulu are at war with each other, as they are with other over the top (OTT) video services like those coming from Apple, Google (YouTube), Disney, and many others.

That battle doesn't interest us - what we are after is the operating system, the guts, that will house all of it. And this is where Roku exists. Each of these over the top (OTT) content providers are available with Roku hardware or software.

The idea behind the business is to grow scale -- to grow active accounts, and to become the operating system of streaming TV. Yes, their goal, their future, is to be what Microsoft was to PCs and what Apple is to smartphones -- the platform, the operating system, for the booming industry that is Streaming Video on Demand (SVOD).

Or, as the CEO said in the earnings call:

Our mission is to be the streaming TV platform that connects the entire TV ecosystem as all TV viewing moves to streaming.

And the company has done so in spades. Not only did ROKU reported a stunning 44% growth in account accounts in Q4, but also an average revenue per user (ARPU) growth of 48%. These are gigantic numbers.

The CEO said, on the earnings call (our emphasis added):

The fourth quarter of 2017 was a fantastic quarter for Roku, reinforcing our leading position in smart TVs, streaming players, OTT advertising and content distribution.

We have never been more excited about the future of our business.

We have never been more excited about the future of our business.

While the company's hardware revenue was down, and that has Wall Street spooked, that was very much on purpose. As the CEO said out loud on CNBC, the company lowered prices on its players to increase volume. It's still a gross margin positive business, but hardware is simply one conduit to more users.

Executives cut the price for one of Roku's top-end models to $100 from $130, for example, and released a budget $30 version called the Roku Express. Again, this was done on purpose. Hardware is a customer-acquisition strategy, not a profit center in and of itself.

Even further, the company noted that for the first time, platform revenue will make up the majority of the company's overall revenue throughout 2018. In fact, platform gross profit grew 120% year-over-year to $63.7 million and represented 87% of total gross profit in Q4, up from 65% last year.

The company gets new users by selling players, licensing players and licensing the operating system. As for other financial metrics, the company's guidance, at its mid-point, is a gross profit rise of fully 56% year-over-year.

Roku's license sources delivered more than half of the company's new user growth in the fourth quarter.

ROKU has access to treasure trove of data and as a distributor of content and an advertiser, data is a key part of that business in the modern world. While ad revenue and content redistribution revenue are the focus, the data behind it is extremely powerful and is a moat that a linear TV cable provider simply does not have.

Think about this, and this is straight from the CEO: "Every ad on ROKU is a one-on-one ad targeted to that specific customer." Now, compare that to cable TV. It's almost an unfair advantage that streaming has over linear television, but there it is.

And the results: advertising remains the largest component of platform revenue, accounting for 75% of that segment, versus 66% in the previous quarter. As for scale, try this on for size:

U.S advertisers spend $70 billion a year on TV, according to ROKU CEO Anthony Wood.

Or how about this: four-years ago ROKU had 0% of the market, and as of last year 1 out of every 5 televisions used the ROKU operating system for streaming. This is much more of a software company than a hardware company, irrespective of where revenue sits today.

Now, let's turn to the earnings results and the earnings call:

EARNINGS

* Revenue: $188.3 million from $147.3 million in the year-ago period, beating analysts' average expectations of $182.5 million.

* EPS: $0.06 profit versus analyst expectations of a -$0.10 per share loss million from $147.3 million in the year-ago period, beating analysts' average expectations of $182.5 million.

* Guidance: Full year revenue of $660 million to $690 million versus estimates of $661.5 million.

Full year losses of $40 million to $55 million versus analyst expectations of $35.9 million.

EARNINGS CALL

Here are the highlights we focused on:

* The shift to streaming is creating huge opportunities for Roku.

* Active accounts grew 44% for the year.

* ARPU increased 48% year-over-year to $13.78 on a trailing 12-month basis with more than two-thirds of ARPU coming from advertising.

* The largest driver of ARPU growth is video advertising.

* We are also seeing very rapid growth from our audience development ads which are endemic display ads.

* Our Roku TV program had exceptional performance, one in five smart TV sold in the U.S in 2017 were Roku TV.

* Our investment and being the leading TV OS is paying off.

* We're increasingly tapping into the $70 billion [] U.S advertisers spend on TV as the TV ad ecosystem moves to streaming.

* More than half of the Ad Age's top 200 advertise on the Roku platform.

* Q4 gross profit increased 64% year-over-year to $73.5 million.

* Platform gross profit grew 120% year-over-year to $63.7 million and represented 87% of total gross profit in Q4, up from 65% last year.

CONCLUSION

We loved the quarter ROKU had, see quite clearly that its actual hardware, which still turns a profit, is not the focus other than as a conduit to get its operating system out there and its account numbers up.

Combine that hardware effort with licensing, and ROKU's growth is something to behold in a cable industry that is flat, at best, and shrinking at worst. Yes, ROKU saw 44% account growth as the cable providers are seeing cord cutting hurt their business.

Advertising is a fantastic business -- just ask Google (the largest advertising platform in the world and the second largest company in the world by market cap) and Facebook (the second largest ad platform in the world and the sixth largest company by market cap in the world).

SEEING THE FUTURE

It's understanding technology that gets us an edge on finding the gems like ROKU that can turn into the 'next Apple,' or 'next Microsft,' where we must get ahead of the curve. This is what CML Pro does.

We are Capital Market Laboratories. Our research sits next to Goldman Sachs, JP Morgan, Barclays, Morgan Stanley and every other multi billion dollar institution as a member of the famed Thomson Reuters First Call. But while those people pay upwards of $2,000 a month on their live terminals, we are the anti-institution and are breaking the information asymmetry.

The precious few thematic top picks for 2018, research dossiers, and alerts are available for a limited time at a 80% discount for $29/mo. Join Us: Discover the undiscovered companies that will power technology's future.

As always, control risk, size appropriately and use your own judgement, aside from anyone else's subjective views, including my own.

Thanks for reading, friends.

The author has no position in ROKU but may initiate one within 72-hours.

Legal

The information contained on this site is provided for general informational purposes, as a convenience to the readers. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation. Consult the appropriate professional advisor for more complete and current information. Capital Market Laboratories ("The Company") does not engage in rendering any legal or professional services by placing these general informational materials on this website.

The Company specifically disclaims any liability, whether based in contract, tort, strict liability or otherwise, for any direct, indirect, incidental, consequential, or special damages arising out of or in any way connected with access to or use of the site, even if we have been advised of the possibility of such damages, including liability in connection with mistakes or omissions in, or delays in transmission of, information to or from the user, interruptions in telecommunications connections to the site or viruses.

The Company make no representations or warranties about the accuracy or completeness of the information contained on this website. Any links provided to other server sites are offered as a matter of convenience and in no way are meant to imply that The Company endorses, sponsors, promotes or is affiliated with the owners of or participants in those sites, or endorse any information contained on those sites, unless expressly stated.