{kind=link}

Intelligent Conditionals: The Volatility Trade After Earnings in Vmware Inc

Intelligent Conditionals: The Volatility Trade After Earnings in Vmware Inc

Date Published: 2018-05-19Disclaimer

The results here are provided for general informational purposes, as a convenience to the readers. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation.

LEDE

To truly optimize trading plans, we need conditionals -- which is a fancy of way of defining the "when." Today we take our trading to the next level, and look at double conditionals.

This is a slightly advanced option trade that bets on volatility for a period that starts one-day after Vmware Inc (NYSE:VMW) earnings and lasts for the 6 calendar days to follow, but then goes one step further, into "conditional" trading. It's this double triggered back-test that we focus on today - intelligent conditionals.

VMW hasn't officially verified its earnings date, but our data provider, Wall Street Horizon has an estimate (unverified) of 5-31-2018.

Vmware Inc (NYSE:VMW) Earnings

In Vmware Inc, especially if the earnings move was up for the stock, if we waited one full trading day after earnings and then bought an one-week strangle (using 14-day options), the back-test results were quite strong. This trade opens one-day after earnings were announced to try to find a stock that moves a lot after the earnings announcement.

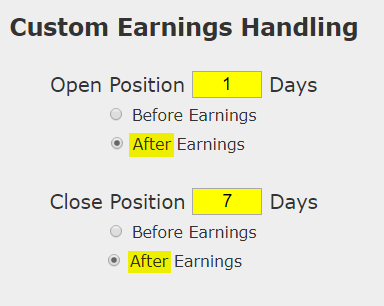

Simply owning options after earnings, blindly, is likely not a good trade, but hand-picking the times and the stocks to do it in can be useful. We can test this approach without bias with a custom option back-test. Here is the timing set-up around earnings:

Rules

* Open the long at-the-money straddle one-calendar day after earnings.

* Close the straddle 7 calendar days after earnings.

* Use the options closest to 14 days from expiration (but more than 7 days).

This is a straight down the middle volatility bet -- this trade wins if the stock is volatile the week following earnings and it will stand to lose if the stock is not volatile. This is not a silver bullet -- it's a trade that needs to be carefully examined.

But, this is a stock direction neutral strategy, which is to say, it wins if the stock moves up or down -- it just has to move.

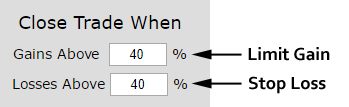

RISK CONTROL

Since blindly owning volatility can be a quick way to lose in the option market, we will apply a tight risk control to this analysis as well. We will add a 40% stop loss and a 40% limit gain.

In English, at the close of every trading day, if the straddle is up 40% from the price at the start of the trade, it gets sold for a profit. If it is down 40%, it gets sold for a loss. This also has the benefit of taking profits if there is volatility early in the week rather than waiting to close 7-days later.

Another risk reducing move we made was to use 14-day options and only hold them for 7-days so the trade doesn't suffer from total premium decay.

RESULTS

When we test owning the 40 delta (out-of-the-money strangle in Vmware Inc (NYSE:VMW) over the last year but only held it after earnings we get these results:

| VMW Long 40 Delta Strangle |

|||

| % Wins: | 75% | ||

| Wins: 3 | Losses: 1 | ||

| % Return: | 333% | ||

Tap Here to See the Back-test

The mechanics of the TradeMachine™ are that it uses end of day prices for every back-test entry and exit (every trigger).

Track this trade idea. Get alerted for ticker `VMW` 1 days after earnings

But, there's more we can evaluate. it turns out that over that same year, if the stock move off of the earnings release was down, this back-test suddenly looks pretty weak. Here are the results when we tested only owning the straddle if the stock move was down.

First the settings:

And now the results:

| VMW Long 40 Delta Strangle Only After a Down Earnings Move |

|||

| % Wins: | 50% | ||

| Wins: 1 | Losses: 1 | ||

| % Return: | 25.2% | ||

Tap Here to See the Back-test

We can see that it has happened twice out of the last 4 earnings sessions, and the results aren't that good. Now, let's reverse this process, and only test this trade if the stock move the day after earnings was up.

First the settings:

And now the results:

| VMW Long 40 Delta Strangle Only After an Up Earnings Move |

|||

| % Wins: | 50% | ||

| Wins: 2 | Losses: 0 | ||

| % Return: | 280% | ||

Tap Here to See the Back-test

Now we see a higher win rate, and a higher average return.

Looking at Averages

The overall return was 280%; but the trade statistics tell us more with average trade results:

➡ The average return per trade was 111.6% over 6-days.

Looking at the Last Two-Years

While we just looked at a single year back-test, we can also hone in on the most recent two-years with the same test -- that is, only testing owning the post-earnings strangle is the stock over the day after earnings was up:

| VMW Long 40 Delta Strangle Only After an Up Earnings Move |

|||

| % Wins: | 80% | ||

| Wins: 4 | Losses: 1 | ||

| % Return: | 315% | ||

Tap Here to See the Back-test

Now we see a 315% return over the last two-years and a 80% win-rate.

➡ The average return for the last year per trade was 52% over 6-days.

➡ The average return for the last year per winning trade was 73.4% over 6-days.

➡ The return for losing trade was -33.7% over 6-days.

WHAT HAPPENED

There's a lot less luck to successful option trading than many people realize. Empirical, objective and explicit results can reveal patterns that show successful trades over and over again.

To see how to do this for any stock we welcome you to watch this quick demonstration video:

Tap Here to See the Tools at Work

Thanks for reading.

Risk Disclosure

You should read the Characteristics and Risks of Standardized Options.

Past performance is not an indication of future results.

Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.

Please note that the executions and other statistics in this article are hypothetical, and do not reflect the impact, if any, of certain market factors such as liquidity and slippage.