{kind=link}

The One-Week Pre-earnings Momentum Pattern With Options in Adobe Systems Incorporated

Adobe Systems Incorporated (NASDAQ:ADBE) : The One-Week Pre-earnings Momentum Pattern With Options

Date Published: 2018-08-17

Disclaimer

The results here are provided for general informational purposes, as a convenience to the readers. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation.Preface

There is a bullish momentum pattern in Adobe Systems Incorporated (NASDAQ:ADBE) stock 7 calendar days before earnings, and we can capture that phenomenon explicitly by looking at returns in the option market.The hardware portion of technology has been hit hard -- Applied Materials and Nvidia guided down, and those two, with Micron, make up the guts of technology. But another part of the industry is doing very well -- it's software and cloud.

Adobe has earnings due out in less than a month -- Wall Street Horizon has an estimate (not a final date) for 9-13-2018. A week before then would put us in early September.

LOGIC

We just looked at a couple of non bullish strategies in the S&P 500 and Amazon, today we look at a directional back-test.The logic behind the option trading backtest is easy to understand -- in a bull market there can be a stock rise ahead of earnings on optimism, or upward momentum, that sets in the one-week before an earnings date.

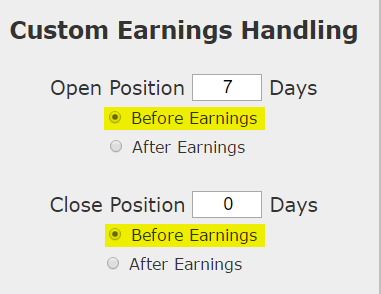

We will examine the outcome of getting long a weekly out of the money (40-delta) call option in Adobe Systems Incorporated 7-days before earnings (using calendar days) and selling the call before the earnings announcement.

Here's the set-up in great clarity; again, note that the trade closes before earnings, so this trade does not make a bet on the earnings result.

Since Adobe reports earnings after the market closes, this back-test does not take on earnings risk. This back-test closes before earnings.

RISK MANAGEMENT

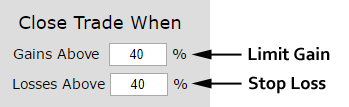

We can add another layer of risk management to the back-test by instituting and 40% stop loss and a 40% limit gain. Here is that setting:

In English, at the close of each trading day we check to see if the long option is either up or down 40% relative to the open price. If it was, the trade was closed. We also back-tested the 14-day options, so there isn't total time decay in the options.

RESULTS

Here are the results over the last three-years in Adobe Systems Incorporated:| ADBE: Long 40 Delta Call | |||

| % Wins: | 83.3% | ||

| Wins: 10 | Losses: 2 | ||

| % Return: | 605% | ||

Tap Here to See the Back-test

The mechanics of the TradeMachine® Stock Option Backtester are that it uses end of day prices for every back-test entry and exit (every trigger).

Track this trade idea. Get alerted for ticker `ADBE` 7 days before earnings

The trade will lose sometimes, but over the most recent trading history, this momentum and optimism options trade has won ahead of earnings.

Setting Expectations

While this strategy had an overall return of 605%, the trade details keep us in bounds with expectations:➡ The average percent return per trade was 36.8% for each 7-day period.

➡ The average percent return per winning trade was 46.3% for each 7-day period.

➡ The average percent return per losing trade was -10.9% for each 7-day period.

Is This Just Because Of a Bull Market?

It's a fair question to ask if these returns are simply a reflection of a bull market rather than a successful strategy. It turns out that this phenomenon of pre-earnings optimism also worked very well during 2007-2008, when the S&P 500 collapsed into the "Great Recession."

The average return for this strategy, by stock, using the Nasdaq 100 and Dow 30 as the study group, saw a 45.3% return over those 2-years. And, of course, these are just 8 trades per stock, each lasting 7 days.

* Yes. We are empirical.

* Yes, you are better than the rest now that you know this.

* Yes, you are powerful for it.

Back-testing More Time Periods in Adobe Systems Incorporated

Now we can look at just the last six-months, as well:

| ADBE: Long 40 Delta Call | |||

| % Wins: | 100% | ||

| Wins: 2 | Losses: 0 | ||

| % Return: | 117% | ||

Tap Here to See the Back-test

➡ The average percent return over the last six-months per trade was 53.8% over each 7-day period.

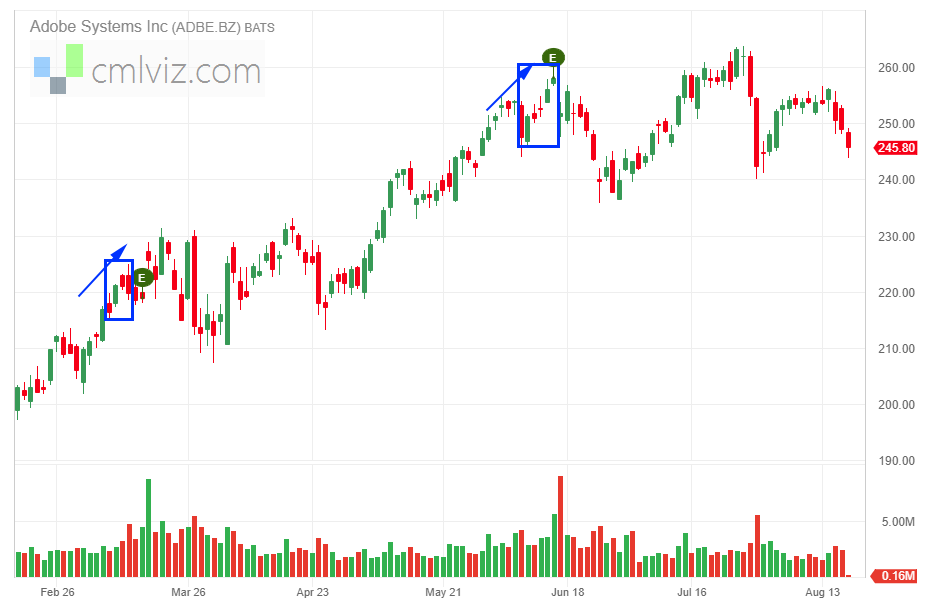

And here's a six-month daily ADBE chart, with the pre-earning momentum highlighted.

Note that the use of a 40% limit in the back-test, turned that first pre-earnings move into a winner with an early exit.

WHAT HAPPENED

In a few mouse clicks and about 30 seconds, we identified a pattern that has repeatedly turned a profit over and over again.Tap Here, See for Yourself

Risk Disclosure

You should read the Characteristics and Risks of Standardized Options.

Past performance is not an indication of future results.

Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.

Please note that the executions and other statistics in this article are hypothetical, and do not reflect the impact, if any, of certain market factors such as liquidity and slippage.