{kind=link}

One on One Interview with Applied Materials CEO Gary Dickerson and Capital Market Laboratories - 'We've never had a demand driver like AI and Big Data'

One on One Interview with Applied Materials CEO Gary Dickerson and Capital Market Laboratories - 'We've never had a demand driver like AI and Big Data'

Date Published: 2019-02-17

Written by Tiernan Ray and Ophir Gottlieb

Hello, all. This is Ophir writing, but most of the story to follow was written by Tiernan. I will add color to the CEO interview with charts and commentary.

LEDE

Top Pick Applied Materials (AMAT) reported a Q1 revenue and EPS beat and Q2 guidance miss but looked forward to, what we believe is, the nearly inevitable future of growth. We remain bullish on the company's future opportunities and CEO Gary Dickerson's vision.

STORY

I will chime in with commentary when appropriate but let's turn to Tiernan's piece and his interview with the CEO of Applied Materials, Gary Dickerson.

Following disappointing earnings forecast for its fiscal second quarter, Applied Materials' chief executive, Gary Dickerson sat down for an interview with CMLviz in which he explained that the changing nature of the semiconductor industry means it's particularly hard to anticipate what the "timing" is of chip purchases.

But Dickerson was upbeat about Applied's role in supplying special materials and special die-stacking technology for years to come.

"The two biggest drivers of our lifetime are Big Data and AI," said Dickerson. "We deeply believe in this next big wave that's coming, and we believe that materials innovation will enable new technologies at the foundation of that wave. I don't think anyone is better positioned than Applied."

Dickerson, who was joined in the interview by his vice president of business operations Tristan Holtam, had two main points to make, one about industry cycles, the other about the changing nature or compute.

On the first score, AI and cloud and Big Data and all these emergent trends in technology are taking over from the smartphone as the driver of the majority of demand for chip making equipment. While that promises lots of new sources of industry growth for Applied and its semiconductor customers, it also means that the timing of buying patterns in chips are less certain than in prior years.

Something as simple as cloud computing data centers are a new set of buyers that change the chip industry demand patterns from what they were when smartphones drove the majority of demand.

"This is the first big inning to this new inflection of the data-centric economy," said Dickerson.

"It's analogous, to me, to what happened with PCs and the emergence of social media," when smartphones first took off, he continued. "I don't know that anyone understood the implications to the industry when that happened."

The other main point Dickerson made was that the entire nature of compute is changing in coming years, to one where chips are more "application-specific" or "workload-specific," for things such as AI tasks in particular.

"The future of computing is going to be different from what it is today," he said. The future of chips is "workload-specific" versus "general-purpose" computing, he said. "We need a 1,000-time improvement in performance per watt ... There is a tremendous opportunity for optimization versus just a general solution."

The breakdown of Moore's Law's two-dimensional scaling tradition, said Dickerson, means not only are new materials required; there will also have to be new architectures in chip design.

"I think it definitely is at a higher level than just process technology," he said. "It involves how you design the systems for power efficiency," said Dickerson. Applied, Dickerson believes, will play an important role in that systems innovation effort, not just in tools for components.

Read the entire Q&A below.

One-on-One CEO Interview

(Our emphasis is added.)

CML: What things are most important for investors to take away from the results and outlook?

Gary Dickerson: For me, what is really driving our business is that if you look at technology, and the impact it will have on our lives in future, we've never been in a better position.

Technology will transform many major industries, from health care to transportation to retail industrial, you can see that a lot of the companies that are growing the fastest today are the companies that have data. That's the value proposition. The two biggest drivers of our lifetime are Big Data and AI. And the foundation of that are semiconductors.

Whether processing or connecting data, we are moving toward a data-centric economy, and semiconductors are at the foundation of that. At the same time, the future of computing is going to be different from what it is today. We need a 1,000-time improvement in performance per watt. We are not going to get there on a linear path.

Everyone sees that 2-D scaling has run out of gas. We need new technology to drive scaling. The foundation of that is materials innovation. We have a new playbook for the industry to drive the future of computing. We have very deep engagements with companies throughout the ecosystem to enable that future. For example, we announced an Engineering Technology Accelerator on the East Coast, and a partnership with IBM for an AI hardware center. Those are initiatives we are driving that align with our view of the future.

It spans materials to systems, from the cloud to the edge. If you think about how you design those systems, the packaging of technology, where there are heterogenous arrangements of structures on a chip, that goes back eventually to equipment and materials.

-- Ophir here. When Gary talks about Big Data, he really means big. Here are some thematic charts to digest:

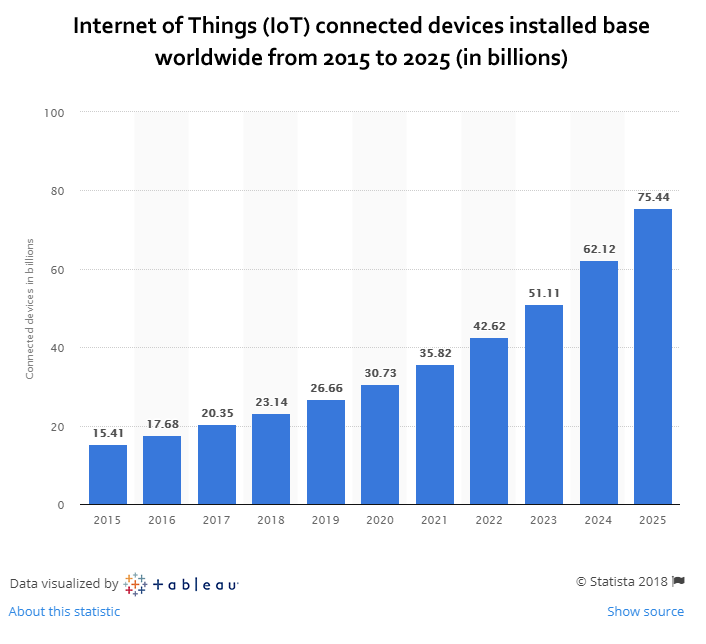

Here's what we know about connected devices, also known as the Internet of Things (IoT):

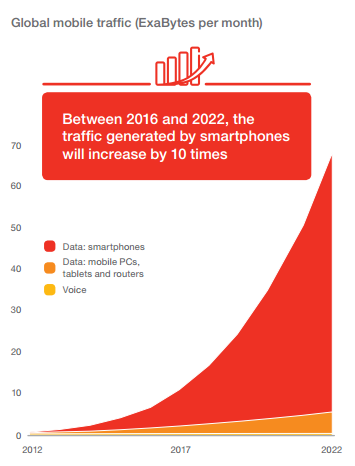

And the image for data creation -- this is just mobile:

We repeat these themes because the best CEOs in the world are repeating them.

Eric Schmidt, the ex-CEO of Google and executive Chairman, said "there were 5 exabytes of information created between the dawn of civilization and 2003, but that much information is now created every 2 days."

We have the broadest set of materials of any company, we can integrate these materials together in any number of ways. I personally spend a tremendous amount of time with all the R&D leaders throughout the ecosystem. That's the biggest opportunity for us throughout the industry going forward.

Near term, everyone can see the downturn in the memory market right now. As that inventory gets worked out - we're not calling the bottom in this call, but at some point, the inventory is going to be worked off, and you will see this economic value in Big Data. You already see it with the cloud services providers.

CML: When you talk about computing being different in future, do you mean changes in chip architecture, or just process technology changes?

GD: I think it definitely is at a higher level than just process technology. It involves how you design the systems for power efficiency. It involves digital and analog computing, how you store and connect the information. How you do all of that at incredibly high speeds and low power.

If you look at the architecture today, and you look at how many of them are not as app- or workload-specific as they will be in future. You see tremendous growth today in many companies building application- and workload-specific designs. But I think the computing architecture on those components will change and how you combine those together will also change.

If you look at power efficiency, if you just scale what we see right now, it consumes an incredible amount of power. That's why we have the Technology Accelerator or the AI Alliance, it's really centered on that focus.

CML: You said in November that the current downturn in the memory market is not like those seen in prior cycles. What do you mean by that?

Tristan Holtam: What we see this time is that the fundamentals in the memory market are a lot healthier. The investments we see in new capacity are a lot more rational than in times past, the players are being a lot more careful from the standpoint of balancing supply and demand, which is very different from cycles of the past five to ten years. As inventories get worked down, the industry is in good shape.

GD: Customers are reacting quickly to the excess inventory. At the same time, you have another factor, which is that you have the cloud service providers now with some level of inventory that they are working through. But I think the customers are definitely reacting quickly.

Looking at demand going forward, with an acceleration in data, we think the customers have ratcheted down spending a very significant amount, certainly memory spending is down a significant amount in 2019. But with the growth in data and storage, there is still a tremendous value to be had.

And you know, we are still seeing evidence of demand elasticity in a lot of these markets. Hard drive prices are going down, and there is an opportunity there for solid state [storage]. The decreasing cost per bit creates opportunities for solid-state.

The long-term demand drivers are very clear in the business. We've never had a demand driver like AI and Big Data. Everyone talks about data being the new oil. It is definitely driving tremendous economic value. We are in the first innings of this information economy. And so for the moment, customers are reacting very quickly, and spending is down very significantly in 2019.

TH: There's maybe a second point to note, with respect to historical trends: we really see a very strong commitment to the technology roadmaps by our customers.

In DRAM, in NAND roadmaps, and in these emerging memory technologies as well, some of which are very important for these new types of computing. In past, it was usually the case that they [chip makers] would back off on the technology investment in parallel to modulating capacity. That's not happening this time. They are sticking with their roadmaps.

-- Ophir here. In our recent dossier on February 6th, 2019 entitled The 'Trillion' Market, we dive deep into the guts of semiconductors. Here are some highlights.

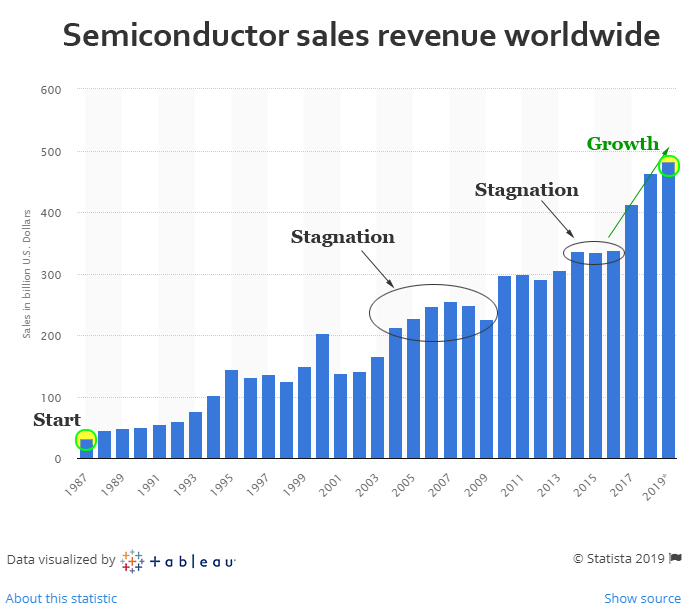

We start with a chart of the entire segment's revenue -- note the volatility when we look myopically, but the overall growth when we look broadly.

It's difficult to miss the pop from 2016, after a few years of stagnation.

Let's get to some more numbers to help fill in the details:

* Memory was the largest semiconductor category by sales with $158.0 billion in 2018, and the fastest growing, with sales increasing 27.4 percent.

Within the memory category, sales of DRAM products increased 36.4 percent and sales of NAND flash products increased 14.8 percent.

We can really think of memory as the initial point from which the new digital economy will launch. Just as demand for memory explodes, so too is the demand for better, faster, more energy efficient and smarter memory.

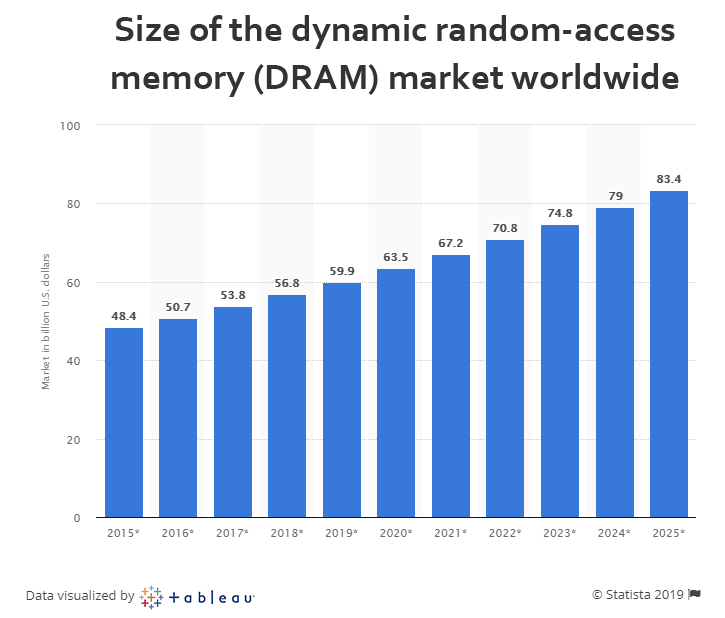

Here is the size of the DRAM market:

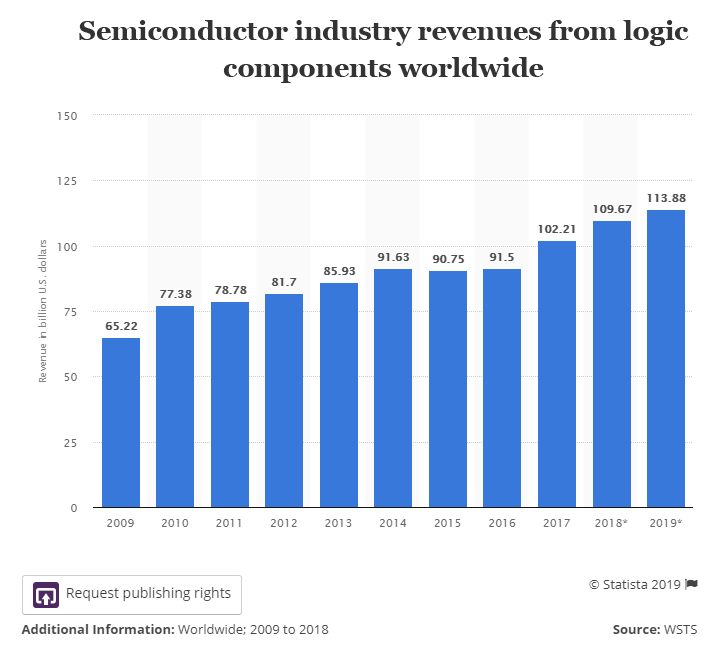

* Logic ($109.3 billion) and micro-ICs ($67.2 billion) – a category that includes microprocessors – rounded out the top three product categories in terms of total sales.

Here is the logic market:

CML: Although there can always be surprises that prompt a turn in any given cycle, it's still somewhat mysterious what this latest downtrend in demand is. Can you explain what happened in 2018 to prompt this current fall-off?

GD: Well, look: Smartphones are down, maybe more than what some would expect. Relative to growth in data centers, that growth is going to continue, there's no question about it, but all of these inflections are, I think, not straight up and to the right.

You will have pauses as people absorb capacity, as they are building out the applications. I think people are still relatively very positive about data disrupting industries. There's been no change relative to the overall strategy.

It's all really part of a new ecosystem. Maybe to some extent there's some learning that has to happen as to how that ecosystem comes together, and the visibility across that ecosystem. We're kind of in this early phase of adoption.

-- Ophir here, again. When Gary speaks about the data center business, we have a lot we can elucidate.

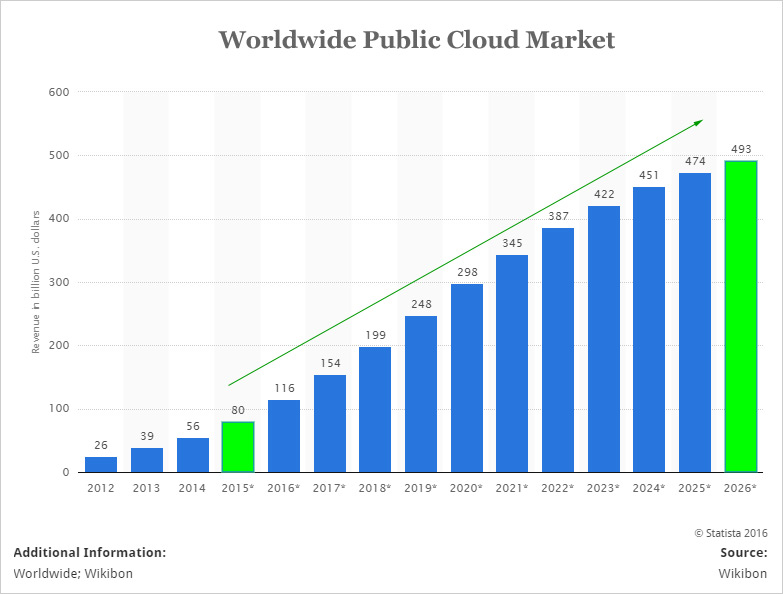

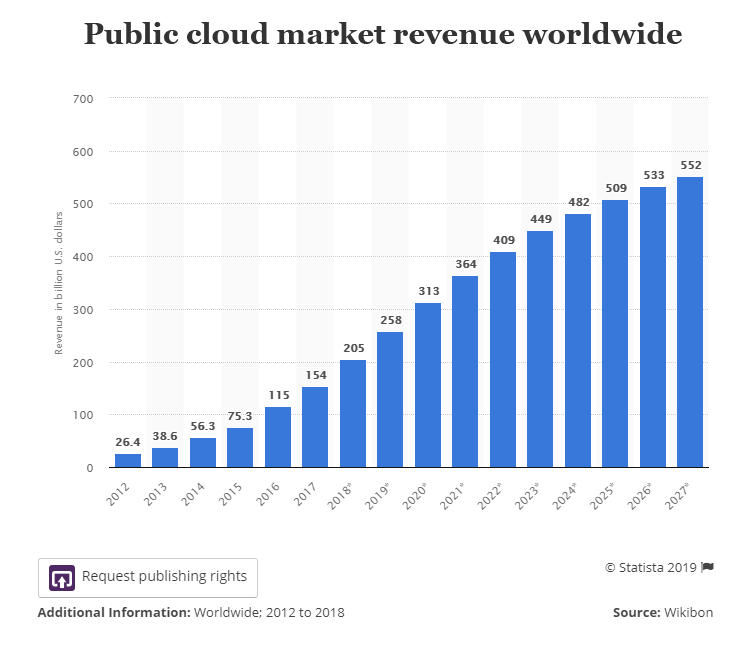

Remember, this was forecast for public cloud market revenue worldwide.

We are one year forward and those numbers have changed. Keep your eyes on 2026 for both charts:

That's right, one year later and Wikibon has upped its forecast from $493 billion by 2026 to $533 billion. Yes, estimates are rising.

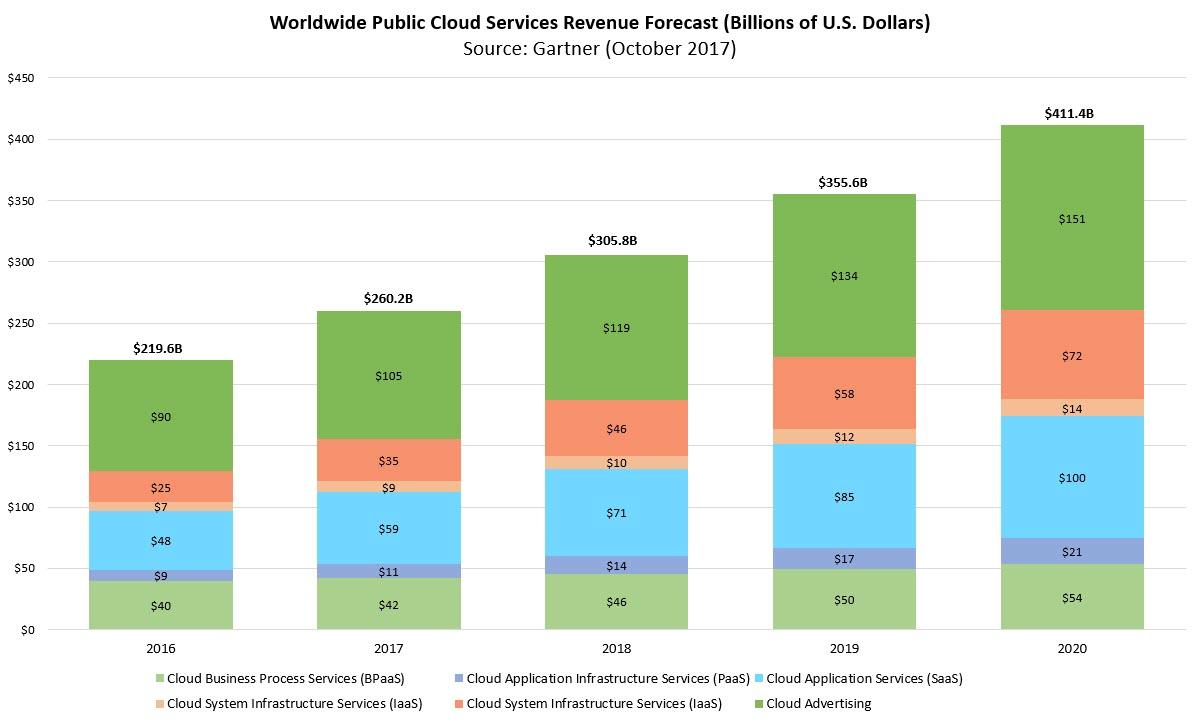

But Wikibon either has not included all revenue sources or it's simply much lower than other research firms. Wikibon pegs the total number for 2020 at $313 billion, Gartner sees it differently, namely, $411 billion.

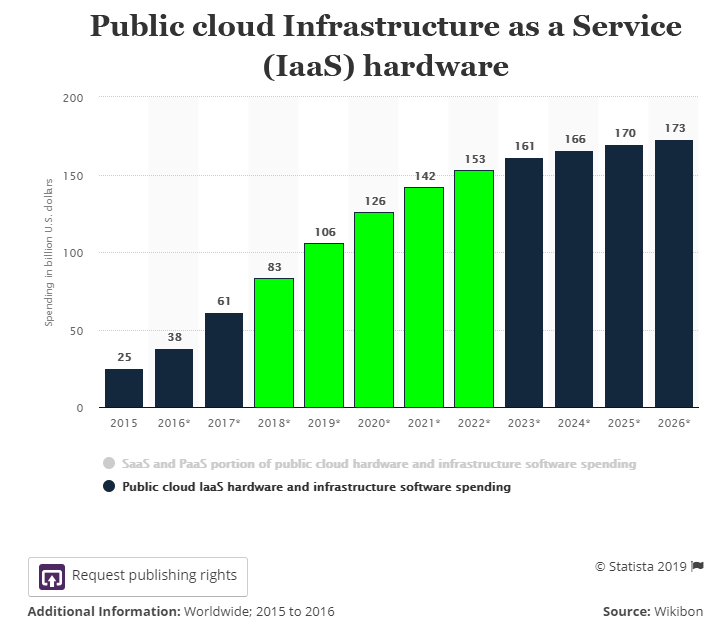

That number is a hodgepodge of several sources. For example, here is public cloud Infrastructure as a Service (IaaS) hardware.

If you take a look at the years 2018-2022, we are on the epicenter of growth.

CML: And perhaps the market you're looking at now is a bit different from a decade ago, when you really had one market, one product, the PC, as the biggest volume driver

GD: You're absolutely right. In the PC case, you were waiting for operating system upgrades. Back then you had a very clearly defined playbook that let you realize the way that the industry worked. That led to huge peaks and valleys.

You would have the operating system upgrade for the desktop, you would have this massive wave of adoption, and then this long pause in between, as people waited, because it was a well-defined cycle. Then we went to the world of mobility and social media, and it was pervasive, and patterns changed in the industry.

Since that time, the volatility has dampened a significant amount. Now, you're going to a world where technology will transform all of our lives. If you look at any of these industries, such as transportation and healthcare and retail and industrial, it's pervasive in many aspects of our lives.

Last year was the first year that more data was generated by computers, humans were surpassed for the first time, all the projections are that, that trend is going to escalate. But, it takes time to build out some of that infrastructure.

To the extent people believe we are heading to a new data economy, the question of who builds that [infrastructure] out first makes a big difference. There's going to be significant infrastructure build prior to those insights. The exact timing of all those different demand drivers isn't exactly clear. You can't dial it into a quarter or a half-year. The direction and magnitude are clear, but you're going to have some perturbations in there.

TH: I'd add to what Gary said by noting that the last five or six years, for WFE [wafer fab equipment, the common measure of aggregate sales in the chip equipment industry], well over 50% of that demand was driven by smartphones.

This year, over 50% is driven by other categories, such as AI, Big Data, cloud data centers, Internet of Things devices, etc. it's a period of transition and diversification. Overall, you are seeing this diversification of drivers of chip demand.

CML: Gary, anything you want to add to that?

GD: Look at this data centric economy, look at what it entails. 5G [cellular]? That's coming. All those new applications you saw at CES [the Consumer Electronics Show trade show in Las Vegas in January], and automotive applications, and all of it, they're all coming.

For the first year now, we are seeing those applications growing to become the majority of demand. It's analogous, to me, to what happened with PCs and the emergence of social media. I don't know that anyone understood the implications to the industry when that happened.

This is the first big inning to this new inflection of the data-centric economy. There are all these industries with fundamental transformation happening. And that's not replacing the other stuff; that's building on top of what came before. PCs are not going away, mobile and social media are not going away. But Big Data and AI are layering on top of what we've seen in the past, increasing the number of demand drivers.

CML: Gary, there's a view in some corners that there are more customers overall for chip making, either because contract manufacturers such as Taiwan Semi are taking on new kinds of customers, or because others want to get into the business of building chips. Either directly or indirectly, there seem to be a rising number of parties that want to make chips, either fab'd or fabless... What do you think about that view?

GD: I think that's exactly right. It comes back to the application-specific workloads we were talking about earlier. Imagine all of the industries or applications where technology will transform those industries - it's a very long list. Companies that aren't in front of that will go away because the nature of competition is changing.

That goes back to the general-purpose-versus-workload-specific-computing discussion. There is a tremendous opportunity for optimization versus just a general solution. For power efficiency and speed, you can optimize a tremendous amount in terms of that workload. You see this all the time relative to people leaving one company and going to another company.

People are building, designing capabilities for application-specific workloads, and the future of computing is changing. It's not going to be driven by 2-D scaling, that will be just one way of driving the future of compute. And this all ties exactly into what you're talking about, people designing new workload-specific technologies.

CML: What can you say about your stock at its current price?

GD: I would think most people think they're undervalued. As CEO you have to have a point of view on the direction and magnitude of the business. We have a very strong point of view relative to the future.

Then it comes back to faith and courage and passion. We have never been in a better position. We deeply believe in this next big wave that's coming, and we believe that materials innovation will enable new technologies at the foundation of that wave.

I don't think anyone is better positioned than Applied, and I don't think anyone has deeper, broader or stronger connections throughout the ecosystems to enable this future.

Personally, for me, I love what I do, and our vision is to make possible technology that enables the future. We want to accelerate many of these changes that make a better future for everyone. We have a deeply meaningful opportunity for Applied and across the globe.

CML: Thanks, Gary.

CONCLUSION

This is Ophir, again. Applied Materials is a growth story, and while demand from quarter to quarter may be lumpy, it is in a leadership position in several segments. We re-iterate our bullish thesis on Applied Materials.

Thanks for reading, friends.

Tiernan has no position in Applied Materials Inc (NASDAQ:AMAT) at the time of this writing. Ophir is long shares of AMAT at the time of this writing.

THE FUTURE

It's understanding technology that gets us an edge to find the "next Apple," or the "next Amazon."

This is what CML Pro does. We are members of Thomson First Call -- our research sits side by side with Goldman Sachs, Morgan Stanley and the rest, but we are the anti-institution and break the information asymmetry. We have five stocks we like even more than Nvidia.

The precious few thematic top picks, research dossiers, and alerts are available for a limited time at a 80% discount for $29/mo. Join Us: Discover the undiscovered companies that will power technology's future.

Thanks for reading, friends.

Legal The information contained on this site is provided for general informational purposes, as a convenience to the readers. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation. Consult the appropriate professional advisor for more complete and current information. Capital Market Laboratories ("The Company") does not engage in rendering any legal or professional services by placing these general informational materials on this website.

The Company specifically disclaims any liability, whether based in contract, tort, strict liability or otherwise, for any direct, indirect, incidental, consequential, or special damages arising out of or in any way connected with access to or use of the site, even if we have been advised of the possibility of such damages, including liability in connection with mistakes or omissions in, or delays in transmission of, information to or from the user, interruptions in telecommunications connections to the site or viruses.

The Company makes no representations or warranties about the accuracy or completeness of the information contained on this website. Any links provided to other server sites are offered as a matter of convenience and in no way are meant to imply that The Company endorses, sponsors, promotes or is affiliated with the owners of or participants in those sites, or endorse any information contained on those sites, unless expressly stated.