Amazon.com Inc.

Amazon May Be The Most Dangerous Technology Company in the World

Fundamentals Technicals | Support: 429.7 | Resistance: Stock is Through Resistance

##Symbol##AMZN

Amazon.com (AMZN) has earnings due out today (July 23rd) after the market closes. While this is a comprehensive look at the company (including "Prime Day" and Jet.com as new competitor), it will focus on why this is the single riskiest earnings event ever for AMZN stock.

AMZN continues to stay at all-time highs with a $225 billion market cap on over $92 billion in sales in the trailing-twelve-months. I will introduce you to the long-term bullish argument and why AMZN is quite possibly the most dangerous and innovative company in the world and is going to change the landscape of our lives in abrupt and amazing ways. While I like Alibaba (BABA), this is where the two firms are totally and completely different. One innovates on a global technological scale, the other innovates on a myopic and internal level.

As promised, we must note what happened on Amazon's first "Prime Day," which was a special sales event for prime ony subscribers ($99 a year). That's a huge driver which I will discuss later. Jeff Bezos and the rest of the Amazon team are laughing heartily at essentially everyone. For a company with such a powerful brand, I don't think I've ever seen such an ugly general disposition on social media about an "idea." "Prime Day" was not just a success, it was the greatest single accomplishment by any technology firm that lives in the on-line sales realm, ever. Lots of details on actual results to follow and why the success of "Prime Day" has actually created unprecedented risk for AMZN.

The first visualization we'll examine plots all tech firms over $30 billion in market cap, equal spaced on the x-axis (i.e. ranked), and with Research & Development (R&D) (in $millions) on the y-axis.

Click Here to Interact With This Image

The company spent over $2.7 billion in the last quarter on R&D which is more than Apple and Google. The spending is trending higher and has seen consecutive increases for 10 straight years on a quarterly basis. While AMZN generates $83,000 in revenue per minute, let's not lose sight of the fact that the firm is disrupting and innovating on a grand scale well beyond on-line sales. Cloud computing is booming and believe it or not, the firm is actually looking at cost controls as it invests in prime subscriptions and streaming media as opposed to hardware. It is seeing substantial margin increases. It is now competing with Netflix (NFLX) both with respect to original content and content redistribution through Prime (like HBO, which is actually available on AMZN).

Earnings Estimates

Revenue: The range is [$21.84 billion, $22.86 billion]. I believe the company will beat the average estimate of $22.37 billion, but my opinion is not of importance for an objective analysis. I do note that some pent-up demand before prime Day may have slowed sales running up to it.

EPS: The earnings per share range is [-$0.61, $0.38] with an average estimate of -$0.14. So yeah, the average estimate is for a loss. I believe the company will beat the average estimate and in fact might even turn a GAAP profit. But again, that's just kind of "finger in the air" guess work, nothing to do with the objective analysis other than cost controls now entering the corporate vernacular. And while I feel pretty confident about a revenue beat, EPS for AMZN is really whacky.

There is a huge risk that even with an earnings beat, the stock could drop because it has risen so far so fast of late and the euphoria of "Prime Day" has been digested. I believe those two phenomena together make this the single riskiest earnings event in Amazon's history. This stock is going to move a lot on earnings, in my opinion.

It's also just about time to talk about this new comer called Jet, which sells items on-line for less than AMZN but simply takes a bit longer to deliver. More on that firm later.

![]()

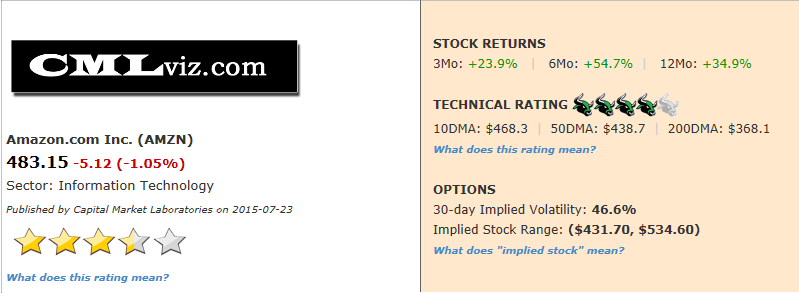

AMZN's 3.10%

rise today is critical to its technical outlook.

Swing Golden Cross Alert: The short-term 10 day MA is now above the 50 day MA.

AMZN has a five bull (top rated) technical rating because it's trading above its 10-, 50-and 200- day moving averages and the stock movement of late has been straight up.

Let's look at the core elements that drive the company's fundamental rating and then we'll dissect them with rspect to this earnings report.

|

|

|

Fundamentals Rating Summary |

|

|

| METRIC | CURRENT | 1YR AGO | 2YR AGO | DIRECTION |

| Revenue (TTM US$ Millions) | 91,964 | 78,123 | 63,978 |  |

| Operating Margin (QTR) | 1.011 | 1.01 | 1.01 | RISING |

| Net Income (TTM US$ Millions) | -406 | 300 | -87 | FALLING |

| Levered Free Cash Flow (TTM US$ Millions) | 3,860 | 2,525 | 798 | RISING |

| Research and Development (US$ Millions) | 2,754 | 1,991 | 1,383 | |

| Research and Development Expense/Revenue | 0.121 | 0.101 | 0.086 | RISING |

|

|

| Stock Returns and Chart |

|

|

Here's a two-year stock chart with regression channel and 10-day momentum (on the bottom).

Click here to interact with this stock chart

Now let's examine the visualizations of the critical financial measures.

| METRIC | CURRENT | 1YR AGO | 2YR AGO | DIRECTION |

| Revenue (TTM US$ Millions) | 91,964 | 78,123 | 63,978 | |

Revenue (TTM) is trending higher meaning that it has increased for at least five consecutive quarters (in this case we're looking at 40 consecutive quarters). Revenue is up 18% year-over-year and 44% over the last two-years. Those are absurd numbers for a company that has basically just failed at entering China and had one of the most embarrassing attempts at a smart-phone ever. For all the greatness of Apple and Google, those two firms rely heavily on essentially one product (the iPhone and search for each respectively). That is not the case with Amazon which has prime, retail, hardware and a cloud computing business.

For this quarter, if AMZN can top $23 billion (which would be a remarkable achievement), the stock could actually rise from here. But, I do think it will take some number like that to push the stock higher in the short-term. That's the revenue side, not the EPS side.

Let's look at Revenue (TTM US$ Millions) in the chart below.

Click Here to Interact With This Chart

Prime Day

Here's what happened, and this is straight from Amazon's press release (with my own emphasis added).

Worldwide order growth increased 266% over the same day last year and 18% more than Black Friday 2014 – all in an event exclusively available to Prime members.

1. Amazon sold more units on Prime Day than Black Friday 2014, the biggest Black Friday ever.

2. Worldwide order growth increased 266% over the same day last year and 18% more than Black Friday 2014.

3. More new members tried Prime worldwide than any single day in Amazon history.

4. Sellers on Amazon that use the Fulfilment by Amazon service enjoyed record-breaking unit sales – growing nearly 300%.

5. Customers ordered hundreds of thousands of Amazon devices – making it the largest device sales day ever worldwide.

6. Members ordered tens of thousands of Fire TV Sticks in one hour, making it the fastest-selling deal on an Amazon device ever.

7. Prime Day was also the biggest day for sales internationally. Customers ordered hundreds of thousands of Fire TV Sticks, making it the best-selling Prime Day product globally.

8. The company sold 398 orders per second.

Remember, this was only available to prime customers -- those people paying $99 a year.

Note: The number one selling product was Amazon's own created hardware. Amazon is a hardware maker, don't forget it. And yes, there will be another attempt at a phone in my opinion (although some have denied that).

There was a wonderful piece from the Washington Post entitled While you were making Prime Day jokes, Amazon was laughing all the way to the bank. There was a sort of indignation by everyone that had never bought the stock and was looking for a reason to watch it go down. But it didn't go down. Indignant or not, people who have not believed in this stock or this company have been dead wrong.

Now, that "Prime Day" stuff has been factored into the earnings estimates so it doesn't mean the stock won't drop, it just means its rise has happened and the company is in position to bully the rest of technology for along time to come. It also means it would take a huge blow out quarter of basically impossible proportions for the stock to rise further in the short-term.

| METRIC | CURRENT | 1YR AGO | 2YR AGO | DIRECTION |

| Gross Margin % | 30.3% | 27.8% | 25.4% | RISING |

The prime business and the cloud computing business (AWS) are much higher gross margin businesses than straight on-line sales. If you're wondering if AWS and prime are working, the answer is clearly seen in this gross margin % trend. We can no longer make the argument that the revenue from those two business lines are trivial if they are moving the needle this much in terms of margins on a revenue base of nearly $92 billion in the last year.

Let's look gross margin % through time in the blue bars. Note that the most recent quarter was the highest ever for AMZN.

Click Here to Interact With This Chart

One thing to keep in mind is that prime membership is huge margin business for Amazon, but the on-line sales that happened on "Prime Day" were likely lower margin than normal. There could be a backward step in margins this earnings release and if you're looking for a sort of short-term bearish thesis, that's a good place to start. If prime membership grew faster than expected because of "Prime Day," then you have the counter argument. Also, AWS is growing at 50% a year and that is a massively high gross margin business.

| METRIC | CURRENT | 1YR AGO | 2YR AGO | DIRECTION |

| Net Income (TTM US$ Millions) | -406 | 300 | -87 | FALLING |

There's no doubt that earnings are an issue with Amazon, and by issue I mean, there aren't any. For the most recent trailing-twelve-months (TTM) the company reported a net loss of -$406 million and the firm has really not seen consistent earnings for three years.

While "Prime Day" was huge, that doesn't mean net income will be better and as I wrote above, it might actually hurt net income if the discounts were, forgive the phrase, "punitive to margins."

In our next chart we plot Net Income (TTM US$ Millions) through time.

Click Here to Interact With This Chart

| METRIC | CURRENT | 1YR AGO | 2YR AGO | DIRECTION |

| Levered Free Cash Flow (TTM US$ Millions) | 3,860 | 2,525 | 798 | RISING |

Levered Free Cash Flow (TTM US$ Millions) is the critical determinant of stock price since market cap (stock price) is the present value of all future free cash flows. For AMZN the metric is up nearly 53% year-over-year and is now at an all-time high of $3.86 billion in the trailing-twelve-months. This number could also take a healthy whack if margin improvement was eroded by "Prime Day." However, longer-term,the fact that "Prime Day" exists is a net positive for Amazon on a grand scale. It will drive prime membership and that's big free cash flow.

For our next chart we plot Levered Free Cash Flow (TTM US$ Millions) in the blue bars.

Click Here to Interact With This Chart

| METRIC | CURRENT | 1YR AGO | 2YR AGO | DIRECTION |

| Research and Development (US$ Millions) | 2,754 | 1,991 | 1,383 | |

Research and Development (US$ Millions) is trending higher meaning that it's been rising for at least five consecutive quarters (in this case it's been 30 consecutive quarters). R&D is now over $2.7 billion in the last quarter, up 38% year-over-year and up a massive 99% in the last two-years. Even further, Amazon's selling, general and administrative (SG&A) expense is also ripping and now stands at about $4.3 billion. Together, those two expenses accounted for about $7 billion in expense last quarter.

I think it’s remarkable that AMZN spends more on R&D than all but three technology companies. That expense (along with Selling, General & Administrative expense (SG&A)) appears to be actually doing something for the firm; the expense is turning into an investment, and that investment is starting to generate returns.

In the final chart we plot Research and Development (US$ Millions) in the blue bars along with SG&A in the gold line.

Click Here to Interact With This Chart

Summary

Amazon has turned the corner and the greatest risk to the stock price is not the company's execution but rather a systematic market correction and a short-term valuation call.

As of right now, regardless of earnings, AMZN is likely the most feared technology company other than Facebook (FB) in that it can enter any market at any time and grab market share quickly without concern for earnings. Further, Amazon, unlike some of its peers, has a well diversified revenue stream that touches its own produced hardware (Kindle, Fire TV Sticks) to cloud computing (AWS), to prime subscriptions and streaming video (which will be a competitive force against Netflix (NFLX)), and of course to on-line retailing.

More "cool" stuff

Amazon has submitted a patent application for its drones. The FAA has granted experimental testing permits to the firm. As CNN so aptly put it, "Delivering packages wherever you want it, through the air, via drone in just 30 minutes -- that's Amazon's vision and the company just made another step forward. [Beyond homes], there's even mention of drone deliveries to boats." Friends, that's downright frightening to any other technology company and beyond. That's downright dangerous. That's downright innovative.

If you believe the expenses are turning into assets and that "Prime Day" was a window into the power of all things Amazon, then you believe the bullish thesis. If you don't, you believe the bearish thesis.

I do note, yet again, that the short-term risk is not trivial given the recent stock rise. Amazon does have a history of reporting some ugly earnings numbers, so let's be prepared for that possibility. For the stock to rise much further, the company would have to report basically "impossible" numbers now that "Prime Day" has been accounted for. But, impossible is possible for AMZN because the company has so much room to cut costs. Even "prety good cost cutting" could spike EPS well into positive numbers (a profit).

Longer-term, this is an incredible company, with an incredible future, an incredible and visionary founder and CEO and clout that few if any companies have in the world today.

Jet.com

Finally, I did promise a window into this new competitor. Here's a great read Amazon Bought This Man's Company. Now He's Coming for Them. The long and short of it is, Marc Lore was the owner of diapers.com which was beaten pretty badly by Amazon, then purchased by the firm. He stayed on for two-years (likely a part of the buyout) and now he has a serious personal vendetta against AMZN. Here's the tagline of the article: "An Amazon veteran is launching a shopping site that's part Costco (COST), part mall, and all anti-Amazon."

He's launching a business very similar to Alibaba (BABA) in some respects and entirely membership fee driven (like Costco (COST)). The goal is to pass savings back to consumers and that means an on-line retail spot that could be cheaper than AMZN. All parties better watch this business evolve and if it has an impact on all things on-line retail, particularly AMZN.