Netflix Inc.

XNAS:NFLX

73.81

+2.91

(+4.10%)

7:59:53 PM EDT: $73.90 +0.09 (+0.12%)

Netflix is Absolutely Crushing It

The Future

Our purpose is to provide institutional research to all investors and break the information monopoly held by the top .1%. Thanks for standing with us.PREFACE

Netflix (NASDAQ:NFLX) stock is down 30% from its highs and it has gone from the best performing stock in the S&P 500 in 2013 and 2015, to an underachiever in 2016 rather quickly.

While the company announced sweeping worldwide expansion, it has seen a drain on free cash flow to fund that expansion and a new round of competitors looking to dethrone it. But, data we received today proves, yet again, that there is one king of streaming video on demand (SVOD), and it's Netflix, without question.

BEARISH ATTACK

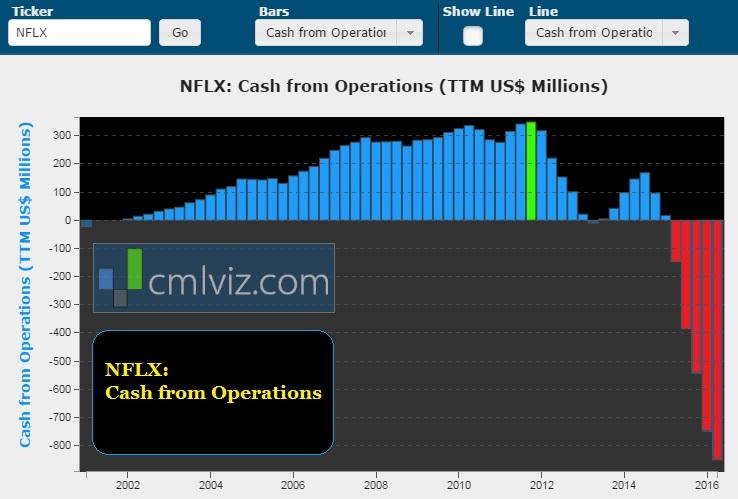

The bearish attack surrounding Netflix can best be illustrated in a chart. Here is the firm's cash from operations for all time:

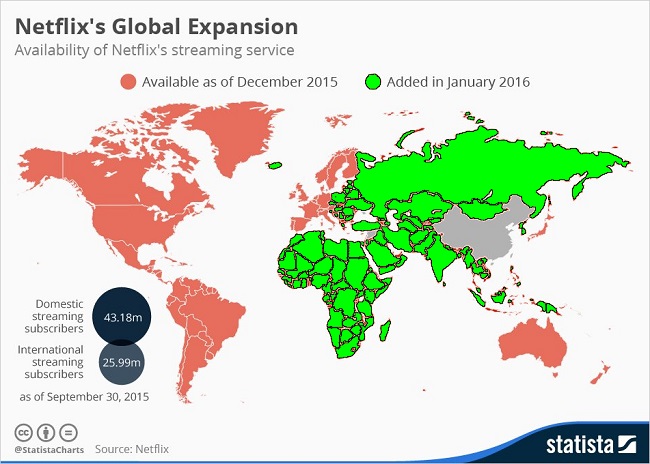

But, while that chart looks like a company in free fall, of course, all of this comes on the heels of Netflix's (NASDAQ:NFLX) unprecedented 130 country expansion announced in January. Here is the company's footprint, with the green areas of the world map representing new markets as of 2016:

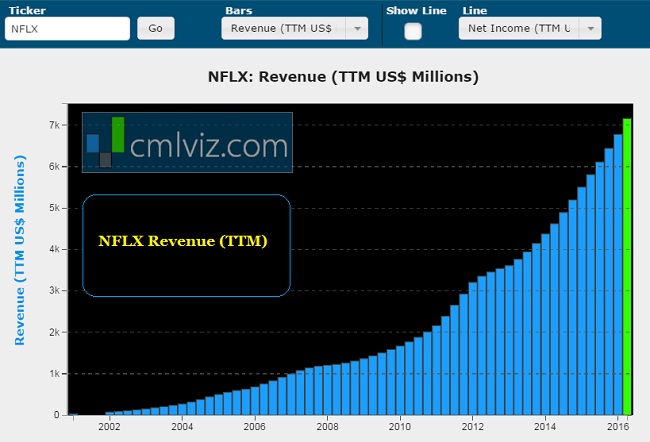

And the evidence, even before today's news, that the expansion is working comes simply from the revenue chart:

Now, here's the breaking news.

BREAKING

The fear of the expansion for Netflix was that it would not be able to grow its brand outside the United States as well as it has stateside. With growth slowing domestically and a huge gamble on international growth, there was reason for worry. Today we learned that the worry was over blown, and so too quite possibly the stock price drop.

Barron's reported that Piper Jaffray's Michael Olson saw positive survey results recently conducted on 2,000 Internet users in Brazil & Mexico. He found awareness of Netflix, as well as intent to subscribe, is high (BARRON'S).

The analyst extrapolated those survey results into some rather lofty expectations:

“

By 2020, we see potential for Netflix to reach ~141M worldwide subscribers, including 63.2M domestic and 77.3M international subs.

Source: BARRON'S

By 2020, we see potential for Netflix to reach ~141M worldwide subscribers, including 63.2M domestic and 77.3M international subs.

”

Source: BARRON'S

That's explosive growth. But Olson isn't on his own here. Barron's also reported that UBS's Doug Michelson reviewed findings of his European colleague, Richard Eary, covering online media on the continent.

“

Netflix is doing quite well across Europe despite intense focus from local competitors in each market, not to mention competition with Amazon (AMZN), who was earlier to enter the U.K. and Germany.

Source: BARRON'S

Netflix is doing quite well across Europe despite intense focus from local competitors in each market, not to mention competition with Amazon (AMZN), who was earlier to enter the U.K. and Germany.

”

Source: BARRON'S

Mitchelson went on to say that "management continues to suggest that only about 20% of international viewing is from local content and that U.S. content continues to travel well everywhere, including in the rest of world markets launched this year."

This is critical because it means that Netflix can focus its spend on US based original content rather than a wild spend on various countries with no substantial estimate as to how each region would do.

Finally, Mark Mahaney with RBC Capital may have been the most bullish. Here are a few snippets

“

1) Very High Usage Levels: 50% now use Netflix to watch Movies & TV shows – down from 53% in February, but same as YouTube (50%) & ahead of Amazon (27%) and NFLX still growing faster than YouTube & Amazon on 2-year basis.

2) Close To Record-High Satisfaction & Record-Low Churn

3) Consistently Improved Content Selection

Source: BARRON'S

1) Very High Usage Levels: 50% now use Netflix to watch Movies & TV shows – down from 53% in February, but same as YouTube (50%) & ahead of Amazon (27%) and NFLX still growing faster than YouTube & Amazon on 2-year basis.

2) Close To Record-High Satisfaction & Record-Low Churn

3) Consistently Improved Content Selection

”

Source: BARRON'S

Further, from his research in France and Germany he found a willingness to pay for streaming content rising materially: 37%/32% of French/ German respondents "Extremely" or "Very" likely to pay for content vs. 21%/20% in December. Further he found rising penetration rates and extremely high (87%) customer satisfaction.

Do you thrive on understanding what's really going on in a company beyond headlines?

Get Our (Free) News Alerts.

COMPETTION

Amazon.com (NASDAQ:AMZN) announced a few weeks ago that it has spun its SVOD service out of Amazon Prime as a stand-alone product. That's simply a direct competitor to Netflix. Further, Alphabet (NASDAQ:GOOGL) Google's YouTube already announced its YouTube Red service -- a premium service for SVOD along with original content spends.

Even Facebook (NASDAQ:FB) announced a standalone SVOD product to compete with YouTube and Netflix and Apple (NASDAQ:AAPL) to has invested in original content for its Apple TV ecosystem.

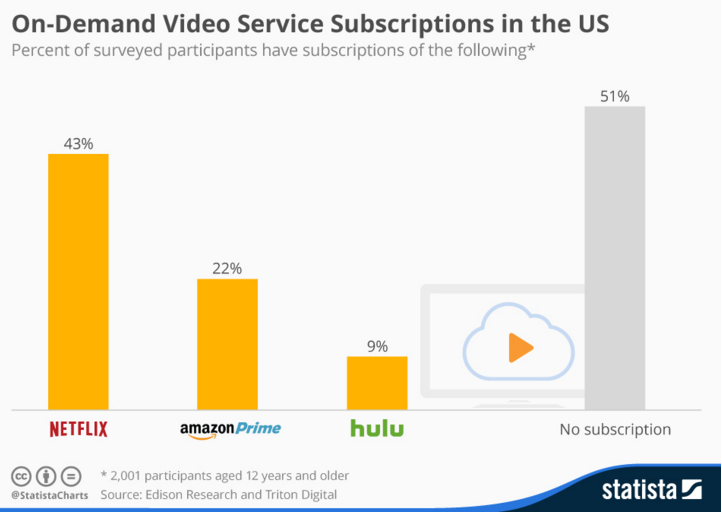

But even given this competition, Netflix maintains a strangle hold on the United States market:

With new evidence from several sources that the Netflix expansion overseas is working, we have to look now at that cash investment and believe that it's worth it and could very well lead Netflix up from its $7 billion base to somewhere near $20 billion in the next five years.

WHY THIS MATTERS

To identify trends like SVOD in the early stages, and then to go beyond, to find the next Apple, Google or Netflix stock, we have to get ahead of the curve. This is what CML Pro does. Our research sits side-by-side with Goldman Sachs, Morgan Stanley and the rest on professional terminals, but we are the anti-institution and break the information advantage the top .1% have.

Netflix is one of just a precious few 'Top Picks' for CML Pro. Each company identified as the single winner in an exploding thematic shift like artificial intelligence, Internet of Things, drones, biotech and more. In fact, here are just two of the trends that will radically affect the future that we are ahead of:

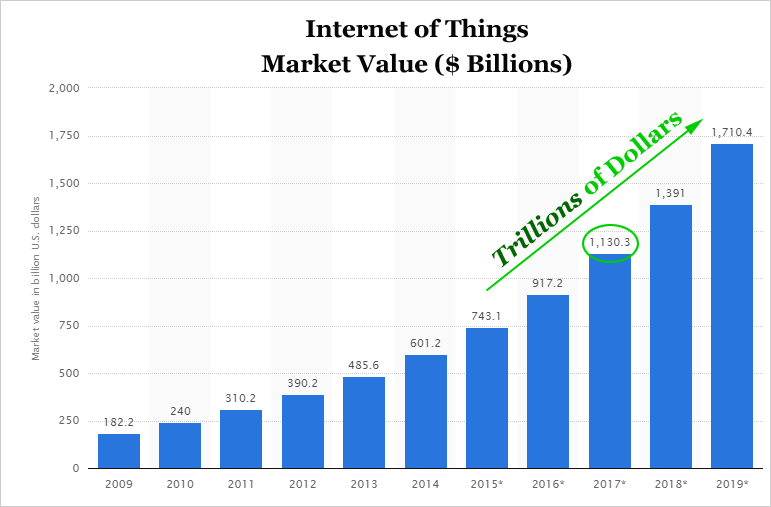

The Internet of Things (IoT) market will be measured in trillions of dollars as of next year. CML Pro has named the top two companies that will benefit.

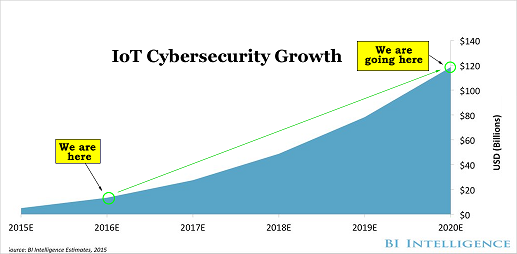

Market correction or not, recession or not, the growth in this area is a near certainty, even if projections come down, this is happening. CML Pro has named the single best cyber security stock to benefit from this theme.

These are just two of the themes we have identified and this is just one of the fantastic reports CML Pro members get along with all the visual tools, the precious few thematic top picks for 2016, research dossiers and alerts. For a limited time we are offering CML Pro at a 90% discount for $10/mo. with a lifetime guaranteed rate. Join Us: Get the most advanced premium research delivered to your inbox along with access to visual tools and data that until now has only been made available to the top 1%.

Thanks for reading, friends.