Regeneron Pharmaceuticals, Inc.

XNAS:REGN 4:00:00 PM EDT

651.18

-24.01

(-3.56%)

: $649.00 -2.18 (-0.34%)

Regeneron Pharmaceuticals Inc, REGN, volatility, earnings, option, before, stock

Disclaimer

The results here are provided for general informational purposes, as a convenience to the readers. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation.

Preface

Regeneron Pharma has had a very bumpy last two-years. Here is a 2-year stock return chart:

We can see the volatility, and if you focus in near the blue "E" icons, you can see the volatility in particular the 14-days before earnings.

It turns out all of those rises and dips have created a repeated pattern. REGN is scheduled to announce its next earnings around 2-8-2018, this is not a verified date yet, but it gives us a time frame. That is, 14-days before then is about January 25th.

The Trade Before Earnings: When it Works

What a trader wants to do is to see the results of buying an at the money straddle two-weeks (calendar days) before earnings, and then sell that straddle just before earnings.

The goal of this type of trade is to benefit from a unique and short time frame when the stock might move 'a lot', either due to earnings anxiety (stock drops before earnings) or earnings optimism (stock rises before earnings), but taking no actual earnings risk.

If the stock is volatile during this period, this generally is a winning strategy, if it does not move, this strategy will likely not be profitable and the complete back-test below discusses that possibility.

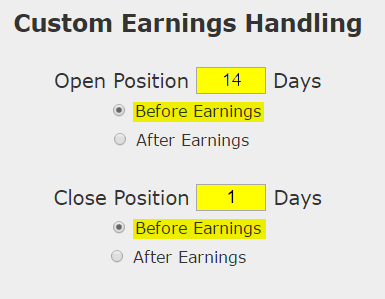

Here is the setup:

We are testing opening the position 14 calendar days before earnings and then closing the position 1 day before earnings. This is not making any earnings bet. This is not making any stock direction bet.

Once we apply that simple rule to our back-test, we run it on an at-the-money straddle:

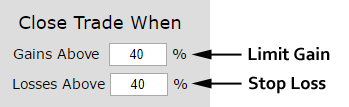

RISK MANAGEMENT

We can add another layer of risk management to the back-test by instituting and 40% stop loss and a 40% limit gain. If the stock doesn't move a lot during this period and the options begin to decay in value, a stop loss can prevent a total loss.

On the flip side, if the stock does move in one direction or another enough, the trade can be closed early for a profit. Here are those settings:

In English, at the close of each trading day we check to see if the total position is either up or down 40% relative to the open price. If it was, the trade was closed.

Returns

If we did this long at-the-money straddle in Regeneron Pharmaceuticals Inc (NASDAQ:REGN) over the last two-years but only held it before earnings we get these results:

Tap Here to See the Back-test

The mechanics of the TradeMachine™ are that it uses end of day prices for every back-test entry and exit (every trigger).

We see a 190% return, testing this over the last 8 earnings dates in Regeneron Pharmaceuticals Inc. That's a total of just 112 days (14 days for each earnings date, over 8 earnings dates).

We can also see that this strategy hasn't been a winner all the time, rather it has won 7 times and lost 1 time.

Setting Expectations

While this strategy has an overall return of 190%, the trade details keep us in bounds with expectations:

➡ The average percent return per trade was 29.4% over each 14-day period.

➡ The average percent return per winning trade was 35.6% over each 14-day period.

➡ The percent return for the losing trade was -13.7% over a 14-day period.

Option Trading in the Last Year

We can also look at the last year of earnings releases and examine the results:

In the latest year this pre-earnings option trade has 3 wins and lost 1 times and returned 45.7%.

➡ Over just the last year, the average percent return per trade was 11.87% for each 14-day trade.

WHAT HAPPENED

We don't always have to look at bullish back-tests in a bull market -- sometimes a straight down the middle volatility pattern pops up. This is it -- this is how people profit from the option market -- finding trading opportunities that avoid earnings risk and work equally well during a bull or bear market.

To see how to do this for any stock we welcome you to watch this quick demonstration video:

Tap Here to See the Tools at Work

Thanks for reading.

Risk Disclosure

You should read the Characteristics and Risks of Standardized Options.

Past performance is not an indication of future results.

Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.

Please note that the executions and other statistics in this article are hypothetical, and do not reflect the impact, if any, of certain market factors such as liquidity and slippage.

{kind=link}

There it is: A Pattern of Volatility Ahead of Earnings in Regeneron Pharmaceuticals Inc

Riding the Clever Pattern of Volatility Ahead of Earnings in Regeneron Pharmaceuticals

Date Published: 2018-01-4Author: Ophir Gottlieb

Disclaimer

The results here are provided for general informational purposes, as a convenience to the readers. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation.

Preface

Regeneron Pharma has had a very bumpy last two-years. Here is a 2-year stock return chart:

We can see the volatility, and if you focus in near the blue "E" icons, you can see the volatility in particular the 14-days before earnings.

It turns out all of those rises and dips have created a repeated pattern. REGN is scheduled to announce its next earnings around 2-8-2018, this is not a verified date yet, but it gives us a time frame. That is, 14-days before then is about January 25th.

The Trade Before Earnings: When it Works

What a trader wants to do is to see the results of buying an at the money straddle two-weeks (calendar days) before earnings, and then sell that straddle just before earnings.

The goal of this type of trade is to benefit from a unique and short time frame when the stock might move 'a lot', either due to earnings anxiety (stock drops before earnings) or earnings optimism (stock rises before earnings), but taking no actual earnings risk.

If the stock is volatile during this period, this generally is a winning strategy, if it does not move, this strategy will likely not be profitable and the complete back-test below discusses that possibility.

Here is the setup:

We are testing opening the position 14 calendar days before earnings and then closing the position 1 day before earnings. This is not making any earnings bet. This is not making any stock direction bet.

Once we apply that simple rule to our back-test, we run it on an at-the-money straddle:

RISK MANAGEMENT

We can add another layer of risk management to the back-test by instituting and 40% stop loss and a 40% limit gain. If the stock doesn't move a lot during this period and the options begin to decay in value, a stop loss can prevent a total loss.

On the flip side, if the stock does move in one direction or another enough, the trade can be closed early for a profit. Here are those settings:

In English, at the close of each trading day we check to see if the total position is either up or down 40% relative to the open price. If it was, the trade was closed.

Returns

If we did this long at-the-money straddle in Regeneron Pharmaceuticals Inc (NASDAQ:REGN) over the last two-years but only held it before earnings we get these results:

| REGN Long At-the-Money Straddle |

|||

| % Wins: | 87.5% | ||

| Wins: 7 | Losses: 1 | ||

| % Return: | 149.6% | ||

Tap Here to See the Back-test

The mechanics of the TradeMachine™ are that it uses end of day prices for every back-test entry and exit (every trigger).

We see a 190% return, testing this over the last 8 earnings dates in Regeneron Pharmaceuticals Inc. That's a total of just 112 days (14 days for each earnings date, over 8 earnings dates).

We can also see that this strategy hasn't been a winner all the time, rather it has won 7 times and lost 1 time.

Setting Expectations

While this strategy has an overall return of 190%, the trade details keep us in bounds with expectations:

➡ The average percent return per trade was 29.4% over each 14-day period.

➡ The average percent return per winning trade was 35.6% over each 14-day period.

➡ The percent return for the losing trade was -13.7% over a 14-day period.

Option Trading in the Last Year

We can also look at the last year of earnings releases and examine the results:

| REGN Long At-the-Money Straddle |

|||

| % Wins: | 75.00% | ||

| Wins: 3 | Losses: 1 | ||

| % Return: | 45.7% | ||

In the latest year this pre-earnings option trade has 3 wins and lost 1 times and returned 45.7%.

➡ Over just the last year, the average percent return per trade was 11.87% for each 14-day trade.

WHAT HAPPENED

We don't always have to look at bullish back-tests in a bull market -- sometimes a straight down the middle volatility pattern pops up. This is it -- this is how people profit from the option market -- finding trading opportunities that avoid earnings risk and work equally well during a bull or bear market.

To see how to do this for any stock we welcome you to watch this quick demonstration video:

Tap Here to See the Tools at Work

Thanks for reading.

Risk Disclosure

You should read the Characteristics and Risks of Standardized Options.

Past performance is not an indication of future results.

Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.

Please note that the executions and other statistics in this article are hypothetical, and do not reflect the impact, if any, of certain market factors such as liquidity and slippage.