{kind=link}

{kind=link}

Option Trading - What Delta is and Why it Matters

Option Trading - What Delta is and Why it Matters

Date Published: 2019-06-11

Disclaimer

The results here are provided for general informational purposes from the CMLviz Trade Machine Stock Option Backtester as a convenience to the readers. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation.What is a 'Delta?"

We have to start with the definition from the Chicago Board Options Exchange (CBOE), but don't worry if this doesn't make any sense, after this formal description, we will explain what delta means in English.Officially: Delta

The amount by which an option's price will change for an one-point change in price by the underlying entity.In English

* A 90-delta option will move about $0.90 for the next $1 move in stock price.* A 50-delta option will move about $0.50 for the next $1 move in stock price.

* A 10-delta option will move about $0.10 for the next $1 move in stock price.

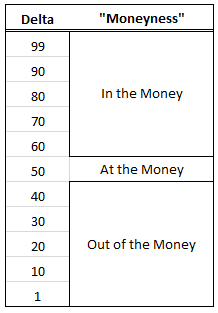

Broadly speaking, 'Delta' measures how far an option is in (or out) of the money and therefore how much it will move for every $1 move in stock price.

Delta ranges from 0 to 1 (or 0 to 100 for one contract since each contract represents 100 shares). The larger the absolute value of delta, the further in the money an option is. In English:

If an option has a delta near 100, it is deep in the money.

If an option has a delta that is near 0, it is far out of the money.

If an option has a delta near 50, it is near the money (at the money).

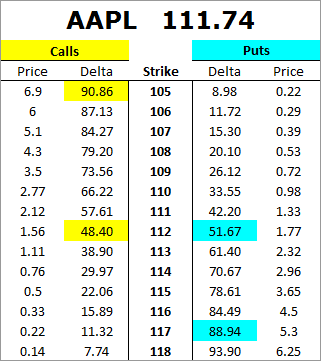

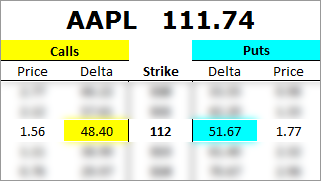

Real World Example on November 29th, 2016

Apple Inc (NASDAQ:AAPL) Stock price in this example is $111.74. Now, let's look at the deltas, strike prices and option prices for a month of options:

First, on the left hand side (in yellow) we see all of the call options.

Second, on the right hand side (in blue) we see all of the put options.

Next to the strike prices, we see the deltas. Let's dive in and focus on one strike price: 105

Stock Price: $111.74

1. The 105 strike call option has a delta of 90.86. This number represents that the 105 call option is deep in the money.

2. The 105 strike put option has a delta of 8.98. This number represents that the 105 put option is far out of the money.

Next, let's focus on the 117 strike.

1. The 117 strike call option has a delta of 11.32. This number represents that the 117 call option is far out of the money.

2. The 117 strike put option has a delta of 88.94. This number represents that the 117 put option is deep in the money.

For completeness, we can look at the options that are at the money.

1. The 112 strike call option has a delta of 48.40. This number represents that the 112 call option is near the money.

2. The 112 strike put option has a delta of 51.67. This number represents that the 112 put option is deep near the money.

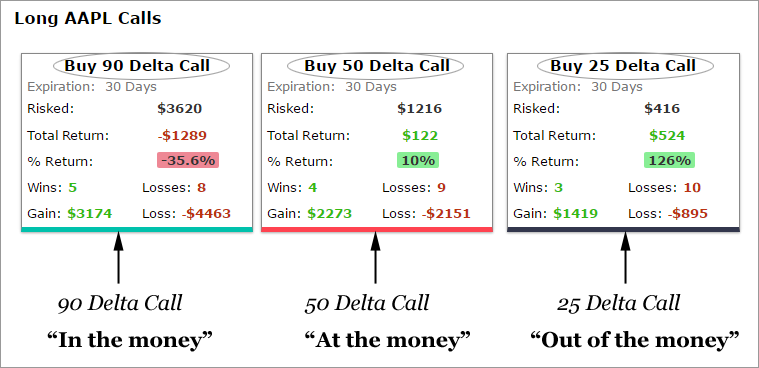

Real World Application in CML Backtester

This is a print out from the CMLviz Option Back-tester:

This example is an one-year back-test, trading every 30 days, for buying a call in AAPL. We can see:

* Buying the 90 delta call (in the money) every 30-days, lost 35.6% over one-year.

* Buying the 50 delta call (at the money) every 30-days, gained 10% over one-year.

* Buying the 25 delta call (out of the money) every 30-days, gained 126% over one-year.

How This Works

(i) The back-tester looks one-year ago, and buys the appropriate delta call option (90, 50 and 25).

(ii) Every 30-days, the backtester sells that call, records the profit or loss, then buys the appropriate delta call option on the new date (90, 50 and 25) again.

(iii) The back-tester repeats this process for a year, trading every 30 days and then presents the results.

Note: The backtester can go back as far as 13-years and can trade as frequently as you desire (even weekly options) and can choose any deltas you want.

DELTA AS A PROBABILITY

Delta is roughly a measure of probability and that's what makes option trading so magnificent.For example, a '30 delta' put should be a winner 30% of the time, or if we sold a 30 delta put, we would expect that we could have a winner 70% of the time. Now, if we can identify a trade that is priced with a 70% win-rate (for example), but find that it wins more often than that, with positive returns, then we have edge - a win that keeps winning.

Watch the demo of the back-tester

Risk Disclosure

Past performance is not an indication of future results.

Trading futures and options involves the risk of loss. Please consider carefully whether futures or options are appropriate to your financial situation. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment.

Past results are not necessarily indicative of future results. The risk of loss in trading can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition.

Please note that the executions and other statistics in this article are hypothetical, and do not reflect the impact, if any, of certain market factors such as liquidity and slippage.

You should read the Characteristics and Risks of Standardized Options.