Symbol not found

:RLYP 00:00AM GMT

0.00

0.00

(0.00%)

Relypsa's Bullish Thesis Goes Further than Takeover Rumors

Relypsa, Inc.

Our purpose is to provide institutional research to all investors and break the information monopoly held by the top .1%.PREFACE

Relypsa (RLYP) is a small-cap clinical stage biopharmaceutical company with a market cap of ~$600 million as of yesterday. Today we're looking at a massive spike to $1 billion.

The company has a single drug named Veltassa that treats hyperkalemia, which is a condition of fatal levels of potassium in patients with chronic kidney disease or heart problems.

Sales of Veltassa officially started in January of this year and in total it is expected to have an addressable market of 2.4 million to 3 million people and to reach peak sales of $1 billion within several years.

BREAKING

Reuters reported that the firm is exploring a sale following a number of overtures from potential buyers, according to people familiar with the matter.

"The discussions are in their early stages and may not lead to a sale, the people added, asking not to be identified because the talks are private."

Relypsa's treatment for hyperkalemia is the first new medicine in fifty years but ZS Pharma has similar compound ready for an FDA ruling this summer.

ZS Pharma sold for $2.7 billion to Astra Zeneca last year. Even with the spike in Relypsa's shares today, the company still sits at a $1 billion market cap.

THE GUTS

Relypsa released its first ever sales update a few weeks ago and then updated it again on March 15th.

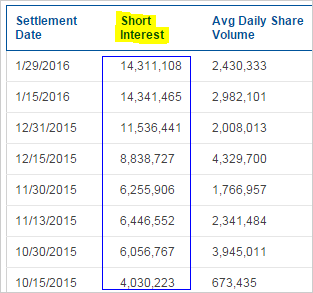

The prescription numbers have been quite good, although the short interest on the stock has punished the price, based on a short thesis that the firm will run out of money by year end and require a financing move.

The stock has enormous short interest. Here's the accumulation:

The drug is doing quite well, awareness is high, demand is high and the drug is welcomed as a much needed alternative. The immense short interest makes for a rather uncomfortable disconnect between the business and the stock.

Every time we get more data on the company, it reads positive. The company announced full month sales for January and February a few weeks ago. We already had data through February 12th, this last update filled in the rest of February.

Bull or bear, the results were quite good.

| Setting | Jan | Feb | % Chg |

| New patients who started taking Veltassa with a free start-supply | 409 | 812 | 99% |

| Outpatient prescriptions reimbursed and dispensed | 99 | 350 | 254% |

| Hospital/institution units sold | 56 | 117 | 109% |

The growth is quite impressive, though we must temper the enthusiasm noting that we are still dealing with small number math.

What was yet more encouraging, is the period from February 12th - February 29th, which was the new data we received, showed no slowing of growth at all.

| Setting | Feb 1-12 | Feb 13-29 | % Chg |

| New patients who started taking Veltassa with a free start-supply | 133 | 217 | 99% |

| Outpatient prescriptions reimbursed and dispensed | 67 | 109 | 248% |

| Hospital/institution units sold | 21 | 38 | 107% |

We also saw, for the first time in a long time, insider buying. My goodness, it's about time. This is from Forbes:

"There was insider buying on Tuesday, by Director Thomas J. Schuetz who bought 30,000 shares at a cost of $13.39 each, for a total investment of $401,832. This purchase marks the first one filed by Schuetz in the past year."

STOCK

The stock has tumbled before today's news all the way down to $13.

At the same time the short interest has accumulated, the closing stock price of $13 (before today) compared to the median price target from all 10 Thomson/First Call analysts of $45, which was a staggering 160% higher . Today the stock is trading near $23.

Further, Wedbush has a price target of $86, H.C. Wainwright has a price target of $63 and Oppenheimer has a price target of $55. Morgan Stanley stands famously as the only firm with a sell rating on the stock.

THE BULLISH THESIS CONTINUES

Agreements have been signed with Express Scripts and CVS Caremark, the two largest pharmacy benefit managers in the United States.

Centers for Medicare & Medicaid Service (CMS) have added Veltassa to its calendar year 2016 Formulary Reference File on Thursday for all three dosage strengths of Veltassa listed on the label. The decision by CMS is both positive and early, with initial expectations calling for a March decision.

This affects about 1.8 million of the 3 million-plus Veltassa-eligible patient population being covered by Medicare (Street Insider).

WHAT'S GOING ON

The Relypsa story is one that seems so bullish and at the same time so steeped in fact that it will feel almost impossible. At the same time, the stock market is never 'wrong,' and the price is tumbling.

THE FUTURE VALUE

Analysts predict that Relypsa's drug will reach peak sales in the United States alone of $1 billion. That's not to speak of Japan, and Europe. As of the close of trading today, Relypsa is trading at a confounding 0.4 price to future sales. The IBB biotech index has an average price to sales of 6 to 1. The stodgy S&P 500 has a price to sales of 2 to 1.

Now, large cap pharma AstraZeneca paid $2.7 billion to takeover ZS Pharma for its hyperkalemia drug candidate. Yes, while we can play the "price-to-sales" game all we want, a major pharma company has said out loud with its pocket book that just the chance of a drug approved in a year to treat hyperkalemia is worth more than $2.7 billion.

Further, a Citigroup analyst said (emphasis added):

"The valuation gap between ZSPH ($2.7B) and RLYP (~$800M) now stands at ~$1.9B, which is embarrassing from a market efficiency perspective for several reasons."

Source: Street Insider

Source: Street Insider

CONCLUSION

Even at a $1 billion market cap, the stock price is now controlled by the massive short interest.

But, at CML, we still hold this company as one of the few gems in small cap biotech with an approved drug, accelerating sales and a large addressable market.

WHY THIS MATTERS

As we said at the top -- if any of the information we just covered feels like a surprise, in many ways it is. But while CML Pro research sits side side-by-side with research from Goldman Sachs, Morgan Stanley, and the rest, we are the anti-institution, and make this type of research available to our retail family for just $10 a month.

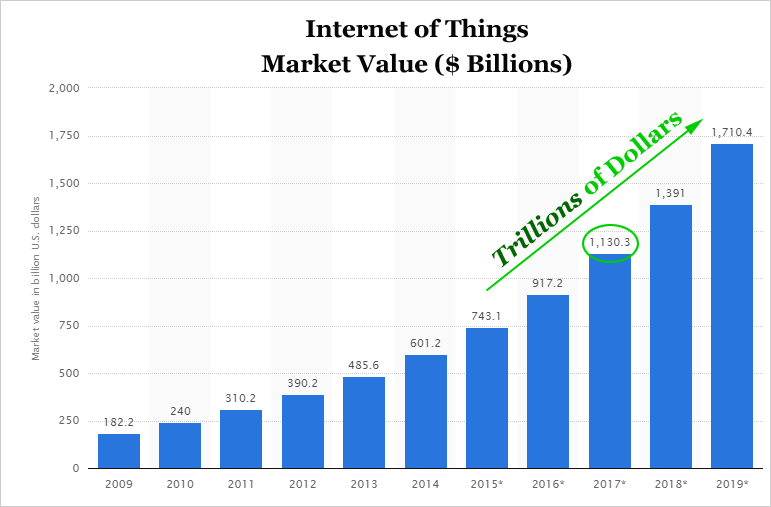

Relypsa is one of just a precious few 'Top Picks' from CML Pro. Each company identified as the single winner in an exploding thematic change like artificial intelligence, Internet of Things, drones, mobile pay and more. In fact, here are just two of the trends that will radically affect the future that we are ahead of:

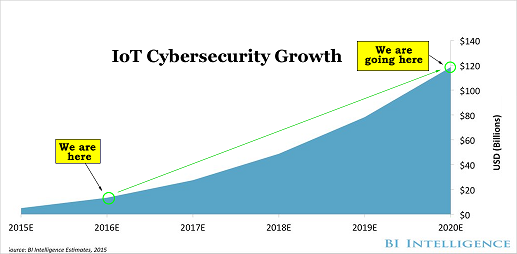

The Internet of Things (IoT) market will be measured in trillions of dollars as of next year. CML Pro has named the top two companies that will benefit. Here's cyber security:

There's just no stopping the growth in the need for cyber security and we are right at the beginning. CML Pro has named the single best cyber security stock to benefit from this theme.

These are just two of the themes we have identified and this is just one of the fantastic reports CML Pro members get along with all the visual tools, the precious few thematic top picks for 2016, research dossiers and alerts. For a limited time we are offering CML Pro at a 90% discount for $10/mo. with a lifetime guaranteed rate. Join Us: Get the most advanced premium research delivered to your inbox along with access to visual tools and data that until now has only been made available to the top 1%.

The author is net long Relypsa.

Thanks for reading, friends.

Please read the legal disclaimers below and as always, remember, we are not making a recommendation or soliciting a sale or purchase of any security ever. We are not licensed to do so, and we wouldn't do it even if we were. We’re sharing my opinions, and provide you the power to be knowledgeable to make your own decisions.

Legal The information contained on this site is provided for general informational purposes, as a convenience to the readers. The materials are not a substitute for obtaining professional advice from a qualified person, firm or corporation. Consult the appropriate professional advisor for more complete and current information. Capital Market Laboratories (“The Company”) does not engage in rendering any legal or professional services by placing these general informational materials on this website.

The Company specifically disclaims any liability, whether based in contract, tort, strict liability or otherwise, for any direct, indirect, incidental, consequential, or special damages arising out of or in any way connected with access to or use of the site, even if we have been advised of the possibility of such damages, including liability in connection with mistakes or omissions in, or delays in transmission of, information to or from the user, interruptions in telecommunications connections to the site or viruses.

The Company make no representations or warranties about the accuracy or completeness of the information contained on this website. Any links provided to other server sites are offered as a matter of convenience and in no way are meant to imply that The Company endorses, sponsors, promotes or is affiliated with the owners of or participants in those sites, or endorse any information contained on those sites, unless expressly stated.